Fixed-to-Float Nearly Narrows the Gap

Written by Flaherty & Crumrine Incorporated

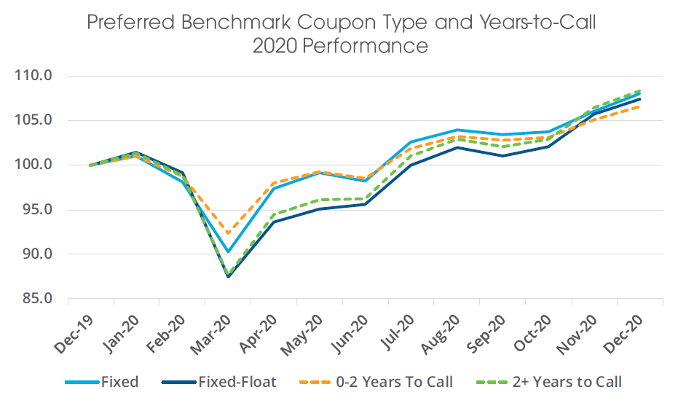

February 18, 2021After significantly underperforming their fixed-rate counterparts during the first half of 2020, fixed-float preferreds have nearly closed the gap, particularly with a strong fourth quarter showing.

To provide some perspective, fixed-float preferreds experienced sharper declines in February and March as declining interest rates and wider credit spreads resulted in projected reset rates that were lower than new issue coupons. Even during the initial months of the recovery fixed-float preferreds remained unloved and investors favored fixed-rate preferreds without the coupon reset risk. However, broad demand for attractive yield and good credit quality narrowed credit spreads significantly over recent months, pushing new issue reset spreads within reach of pre-pandemic levels. With new issue coupons also significantly lower, fixed-float preferreds looked attractive again, particularly given their generally longer call protection which is critical for protecting income in a low yield environment.

The importance of call protection when most preferreds trade above par value can be understood through a simple illustration. Suppose there are two securities that are identical in all respects except call protection. Both are priced at 105 and can be called at their par value of 100. Between now and when they are called, the price on both will decline to 100, resulting in a roughly 5% price loss. However, the security with longer call protection will spread this 5% price loss over a longer period of time, resulting in a higher economic yield. Therefore, at any given price above par value, the yield-to-call will be higher for a security with longer call protection, precisely because the price premium will be amortized over a longer time period.

As we look forward to 2021, we believe longer call protection will be crucial in a low yield environment where most preferreds trade above par value and the likelihood of call is high. Fixed-rate preferreds typically have shorter call protection so their price is more constrained by the issuer’s ability to call the security at par value (negative convexity). In contrast, with their typically greater call protection, prices on many fixed-float preferreds can move higher with a longer runway to amortize price premiums. Additionally, longer call protection allows a portfolio to postpone reinvestment at today’s lower yields and therefore maintain more stable income.

Destra Capital Investments is providing this update with permission from Flaherty & Crumrine, Incorporated. No offer or solicitation to buy or sell securities is being made by Destra Capital Investments.