Green on the Screen!

April 1, 2024As if St. Patty’s Day was not enough, there was green all over the screen in the month of March and for the first quarter of 2024. It has been a wonderful time to be long risk assets! Stocks, credit, alts, … you name it, have all surged in the first quarter of the year. Despite major news stories, political intrigue, wars, trade and supply route disruptions and near gridlock in Washington (or maybe, paradoxically BECAUSE of gridlock in Washington) the markets have marched forward and most account balances will show big increases for people when the March 31st statements hit client mailboxes here the first week of April.

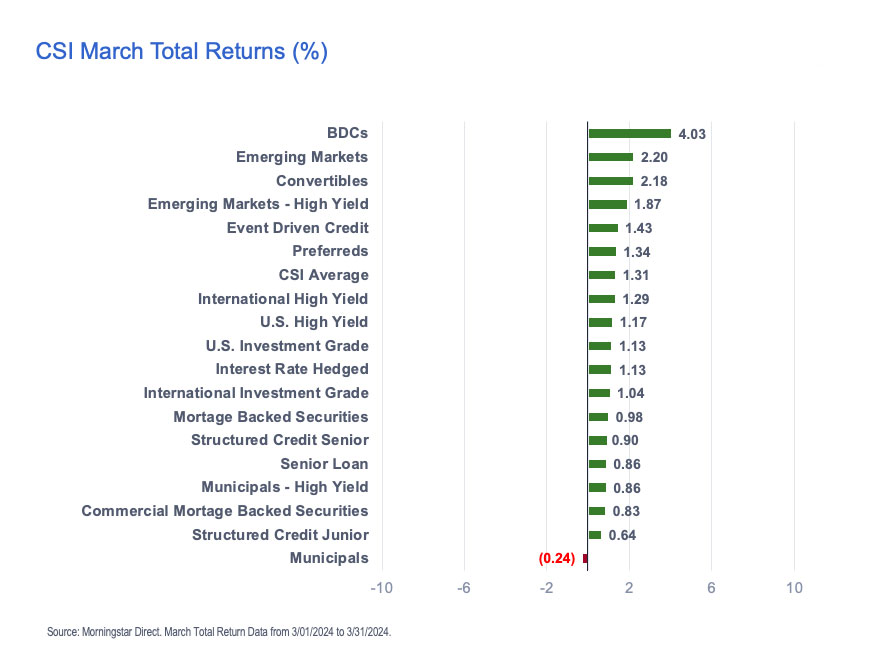

The Destra Credit Strategies Indicator (“CSI”) was nearly solid green in the month of March, with 17 of 18 categories in positive territory. The BDC category took the lead yet again, up an astonishing 4.03% for the month of March alone. It was joined in the top ranks by Emerging Market Debt, up 2.20% and Convertibles, up 2.18% respectively for the month.

On the other end of the scale, Municipals were the only CSI category in the red for March, losing (-0.24%). The Structured Credit Junior category managed a positive 0.64% but was the second worst performer in the CSI for the month, with CMBS strategies rounding out the bottom three, up 0.83%.

First Quarter Results

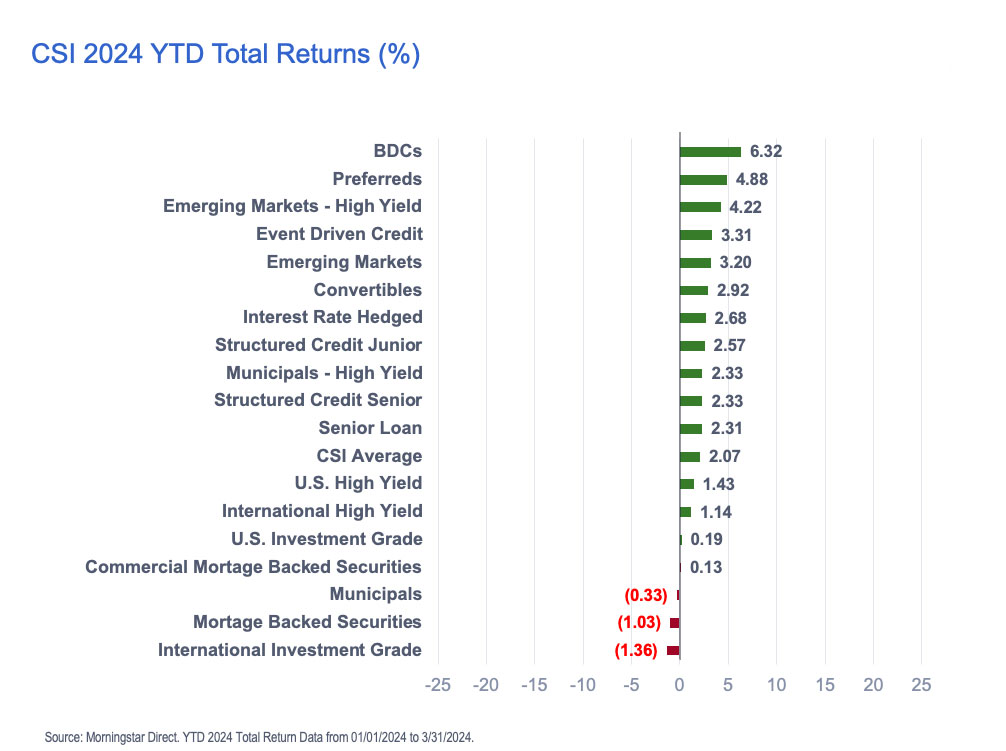

Looking at CSI results for the entire first quarter we see that the BDC category is the top dog at 6.32%, followed by Preferreds at 4.88% and Emerging Market High Yields at 4.22%. Can someone say, “RISK ON”?

Preferreds have modest rate risk in today’s structures, but they are subordinated to more senior debt at the issuing firms, which are typically investment grade corporations. BDCs on the other hand are generally creating loans for smaller, mid-market companies that would almost certainly be excluded from more traditional sources of debt financing in the market. To say that these two are at opposite ends of the credit quality spectrum would be an understatement. Yet here they are, in the top two spots for total return in credit strategies year to date.

But all is not right with the credit world to start 2024. The International Investment Grade credits have started the year down (-1.36%). Both Municipals (-0.33%) and Mortgage Backed Securities strategies (-1.03%) are in negative territory as well. Interestingly, this might suggest that higher quality bonds like Investment Grade and Municipals, don’t have enough "umph" in them right now to attract buying pressure and support prices on top of their coupon. "Umph" is a very technical investment term roughly translated in finance speak to ……spread!

Spring Is In The Air….You Can Smell The Credit Fires!

Spring is indeed in the air here in early April and lawyers are in love…..in love with filing Chapter 11 bankruptcies. Since the Fed began raising rates in 2022, there has been a trend up in bankruptcy filings, but it has really taken off here in early 2024.

And it appears that there is more where that came from as “Fed hikes are increasingly impacting coverage ratios for highly leveraged companies…,” according to the team at Apollo.

Bloomberg had an article https://www.bloomberg.com/news/articles/2024-03-25/junk-market-flashes-warning-as-fed-eyes-higher-rates-for-longer in the last few days of March that walked through the gut check hitting leveraged finance from rates staying higher for longer.

All of which brought out this comment from RBC BlueBay Chief Investment Officer, Mark Dowding this week,

“…amidst the enthusiasm, it is worth highlighting an uptick in credit events in the high yield space. In Europe, for example, we see distressed trading and likely restructuring events in names such as Altice, Intrum, Ardagh, Grifols. This again serves as a remainder of the importance of credit selection and proper diversification. For sure, it is never a great outcome when investor attitudes grow too complacent in credit.” (emphasis Destra’s)

Will the rest of 2024 be as kind to credit strategies as the first quarter has been? It seems that there are clearly stresses in the system as Apollo, Bloomberg and RBC BlueBay point out above. Investors would do well to keep an eye on company fundamentals as much as they do on where central banks might take short term rates. These are different risks to be sure but being too myopic about one (rates) could leave an investor blind to the other (credit).

We will be back next month to update you on how credit strategies perform through April. Until then, if you would like to learn more about Special Situation investing, we recommend you download a special whitepaper HERE, from Destra. We are happy to provide this detailed look at a very unique, high value credit strategy.