Investment Grade Bonds Suffer While Spread Strategies Shine

Destra Capital

March 1, 2024Through the first two months of 2024, Intermediate Treasuries are off some 85bps on return and the Bloomberg US Agg index is off even more, at -1.68%. These two hallmark benchmarks represent the biggest portions of the bond investing landscape and if you only used these as a gauge you might say that fixed income investing was off to another poor year.

But away from Treasuries and Investment Grade credit, many credit strategies are doing well on a total return basis to start 2024.

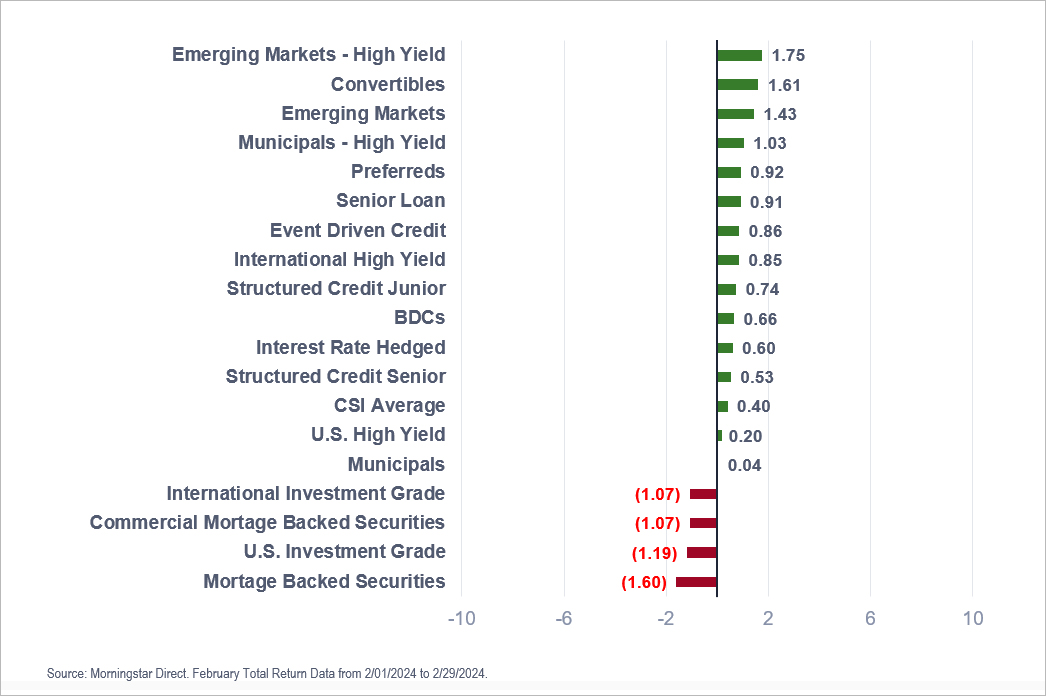

In February for example, the Destra Credit Strategies Indicator (“CSI”) had 14 positive sub-strategies and only 4 negative in the month. Positive contributors were led by emerging market debt strategies, while convertibles, high yield munis, and preferreds were the next best performers rounding out the top 5. Interestingly, US high yields, although positive for the month, were almost 150 bps behind emerging market high yield and some 65 bps behind their international cousins in February.

Duration Boomerang

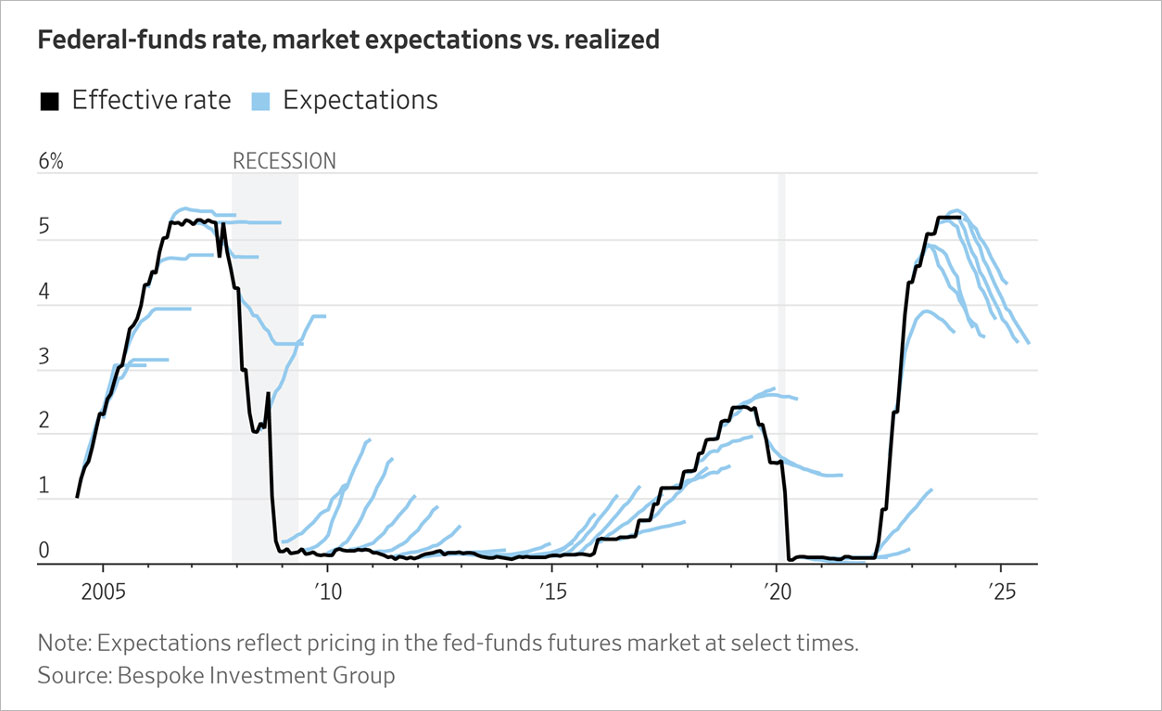

Many investors came into February thinking the Fed would soon be cutting rates and thus they were on the hunt for duration. But as February wore on, the inflation numbers and persistent strength of the US economy began to wear on longer duration strategies in the CSI, such as investment grade corporates and mortgage-backed securities.

Bankruptcies Down, But Recoveries Are Too

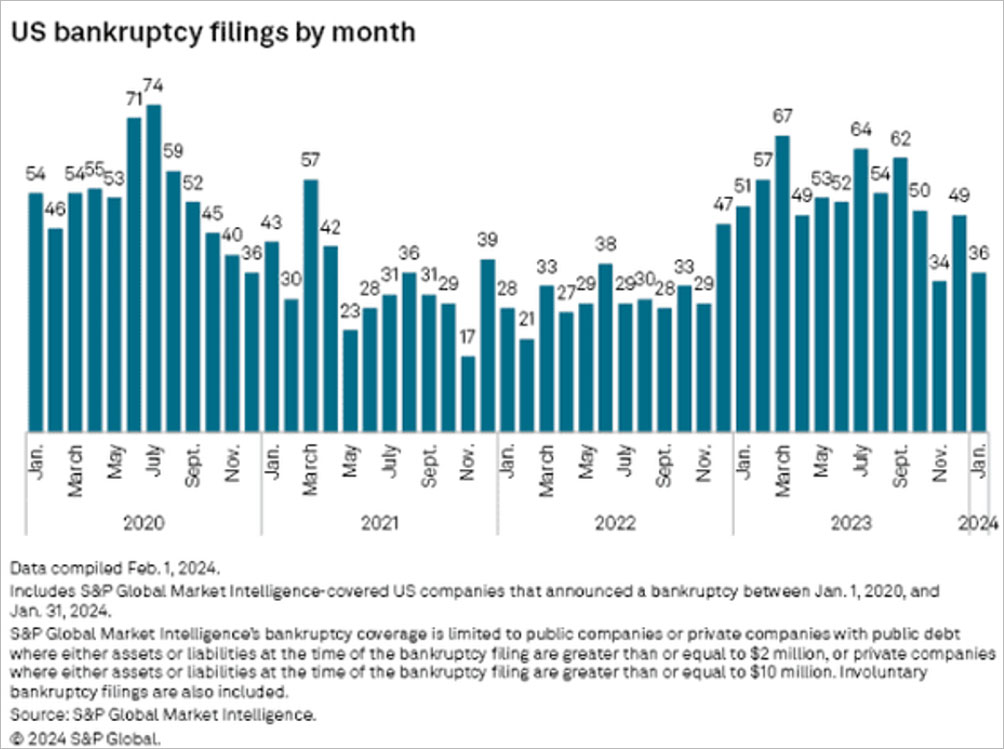

There is a lot of talk about higher base rates putting stress on companies that have to refinance, especially in the high yield and senior loan markets. But bankruptcies actually started off the year slow in January compared to 2023.

One month does not a trend make, so bankruptcies and defaults may yet pick up as we move through 2024, but another metric in the risky end of the leveraged financial pool does not bode well for credit investors.

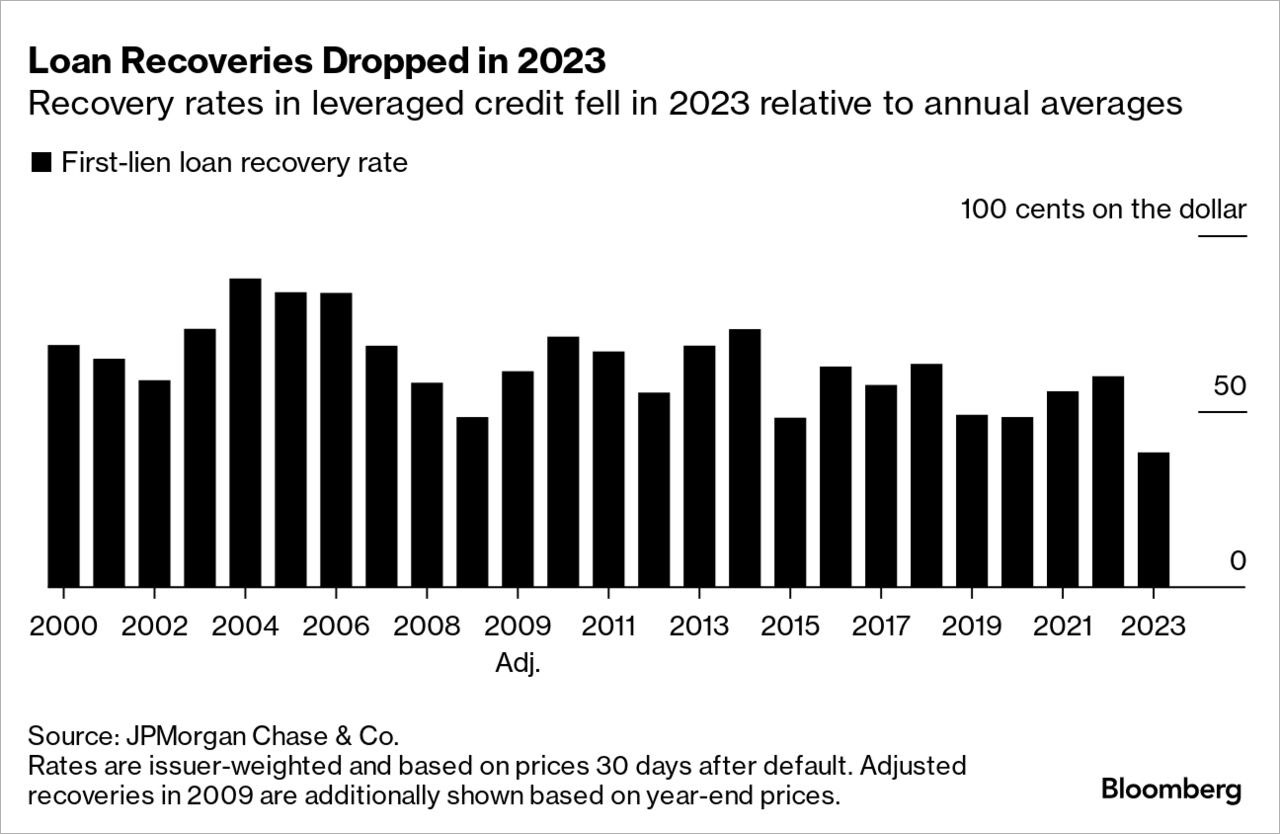

Last year, those loans that did hit the skids, were difficult to extract recoveries from. In fact, first-lien loan recoveries from defaults in 2023 hit a 23 year low!

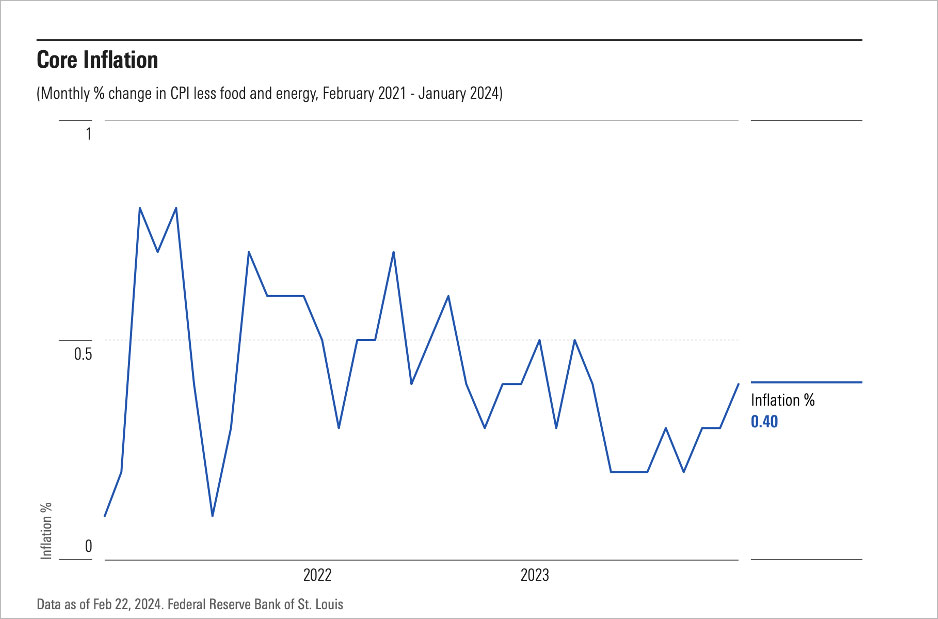

Core Strength

And if you were holding out hope for falling rates to take the burden off credits that are coming under stress, you might want to think again. Frankly, the core inflation numbers from the US economy do not suggest that the Fed will be in any rush to pull back on short term rates soon.

The CPI (less food and energy) has been heading in the wrong direction the last few months. That is not going to make it easy for the Fed to start cutting rates. In fact, it is doing the opposite. Unless this trend reverses quick, we can say goodbye to the idea that the Fed funds rate is coming down anytime soon.

By the way, follow this link for a short, but excellent article on CPI from Morningstar https://www.morningstar.com/economy/how-read-cpi-report.

We hope you found this edition of our monthly Credit Events interesting. If you would like to receive our occasional long-form version, click HERE. Our latest report is an in-depth interview with a stressed and distressed investing expert, where we get his views on what opportunities are out there for investors willing to sift through the wreckage of special situations.