Preferred Market Update

March 16, 2020A selloff in preferred and contingent capital securities, alongside corporate and high-yield bonds, accelerated last week as coronavirus fears intensified. Rising cases of Covid-19 outside China, lockdowns in Italy, Spain and France, a patchwork of federal and state government responses, and limited availability of coronavirus testing in the United States gave investors plenty to worry about.

We are not epidemiologists and cannot opine on the particular course of the current coronavirus pandemic, although a sharp decline in new Covid-19 cases in China suggests strong efforts to limit transmission can be effective. As investors in long-term (often perpetual) securities, we have always taken a long view on the economy, credit quality and an issuer’s ability to meet its obligations. From that perspective, we remain confident in the preferred market in general and our investments in particular. We outline our reasoning below.

First, monetary policy has eased and is likely to continue to do so. Central banks globally have cut rates and, more importantly, are providing liquidity to their banking systems. We will focus on the US, but many foreign central banks have taken similar steps as well.

- Rate Cuts. In the US, the Federal Open Market Committee (FOMC) got things started with a 50 bp rate cut on March 3, two weeks ahead of its regular meeting on March 18, and increased repo operations from prior levels to sustain lower target rates. It followed that up on March 15 with a 100 bp cut in coordination with the central banks of Canada, England, Japan, Europe and Switzerland (more below). The fed funds target range is back to its financial crisis low of 0‑0.25%.

- Repo Liquidity. On March 12, the Fed expanded repo operations to offer $500 billion in 3-month repo funds and $175 billion in overnight repo. The Fed will offer on a weekly basis $500 billion of 1-month and 3-month repo funding in addition to offering $175 billion in daily overnight repos. These will continue at least through April 13, and it’s very likely they will continue until coronavirus concerns have been significantly reduced.

- Discount Rate Cuts. Going even farther than its funds rate cuts, the FOMC lowered the discount rate to 0.25% effective March 16, eliminating a 50 bp premium over the top of the fed funds target range. Discount window borrowing is available to a larger group of banks and can be collateralized by a broader range of collateral than repo operations. Moreover, the Fed is encouraging banks to use the discount window and wants to remove any lingering “stigma” to its use that prevailed before the 2008-09 financial crisis. This helps ensure that all banks have access to liquidity for lending.

- Renewed Quantitative Easing (QE). On March 13, the Fed resumed QE by buying a range of Treasury maturities (not just Treasury bills) as part of its $60 billion in monthly reserve additions it previously announced. Just two days later, the Fed announced it will purchase at least $500 billion of Treasury securities and at least $200 billion of agency mortgage-backed securities “over coming months.” It will also shift reinvestment of the portion of maturing mortgage proceeds that had been going into Treasuries back into agency MBS. These actions will add to reserves, support Treasury market liquidity and enhance transmission of rate cuts to consumer mortgage rates (i.e., promote mortgage refinancing).

- Dollar Swap Lines with Foreign Central Banks. On March 15, the Fed announced lower rates and longer terms on swap lines with the central banks of Canada, England, Japan, Europe and Switzerland. There have been strains in global markets for US dollar funding recently, and this change should help alleviate that.

- Other Measures. The Fed announced it will encourage banks to use a portion of their capital and liquidity buffers to support lending. In a practical sense, that means letting banks run smaller cushions to regulatory minimums than they might have in the past.[1] In a related move, eight large US-based global systemically important banks (G-SIBs)[2] announced they will suspend share repurchases through the second quarter of 2020 and redeploy that capital to support lending.

Eliminating Bank Reserve Requirements. Effective March 26, the Fed is eliminating reserve requirements for depositary institutions. While this is largely a technical change, it’s another way to free up reserves that can be made available for lending.

These are broad and substantive actions by the Fed and other central banks. The Fed’s provision of liquidity and lowering of constraints on banks to deploying that liquidity are particularly important. As governments, businesses and individuals seek to slow the spread of this virus, the economy’s demand side (e.g., reduced travel & entertainment spending, deferral of investment spending) and supply side (e.g., reduced work hours and business closures, supply chain disruptions) will come under downward pressure. If measures to slow viral transmission are successful, reductions in economic activity should be temporary, but they could be sharp. US inflation-adjusted gross domestic product (real GDP) is almost certain to be negative in the second quarter. Businesses will need working capital and an ability to refinance maturing debt during this period, so it’s critical for the banking system to be able to supply that credit. Similarly, individuals may see work hours curtailed and face strains meeting debt obligations; they will need forbearance. Banks in the US are exceptionally well-positioned to do that, with strong levels of capital and large loan-loss reserves. And the Fed is ensuring that banks have ample liquidity to meet demand for credit. This is how monetary policy prevents a serious but inherently short-term disruption from becoming a long-term downturn – and the Fed is getting ahead of this problem. We think it’s highly unlikely that Covid-19 precipitates a financial crisis in the United States.

Second, the US economy comes into this situation in good shape. Real GDP growth was 2.3% last year, and the Atlanta Fed’s most recent “nowcast” for first-quarter GDP is 3.1% (updated 3/6/2020 reflecting data mostly from January and February). Of course, economic activity likely slowed significantly in March and probably will be even worse in April. However, the US economy faces coronavirus shocks from a position of strength, and monetary policy and, increasingly, fiscal policy should help soften the blow.[3]

Turning now to markets, as the Fed cut rates to near zero, Treasury yields fell sharply. The 10-year Treasury today yields about 0.7% compared to 1.6% in mid-February before coronavirus concerns began to intensify and 1.9% at the end of 2019. After its latest move, Fed Chairman Powell commented that the FOMC would be “patient” in raising the funds rate. We expect rates will remain exceptionally low until a coronavirus vaccine has been developed and administered widely, which health officials expect will take at least 12 months. Accordingly, short-term rates should stay low for the next year or more, though intermediate and long-term rates could move up as progress fighting the virus is achieved.

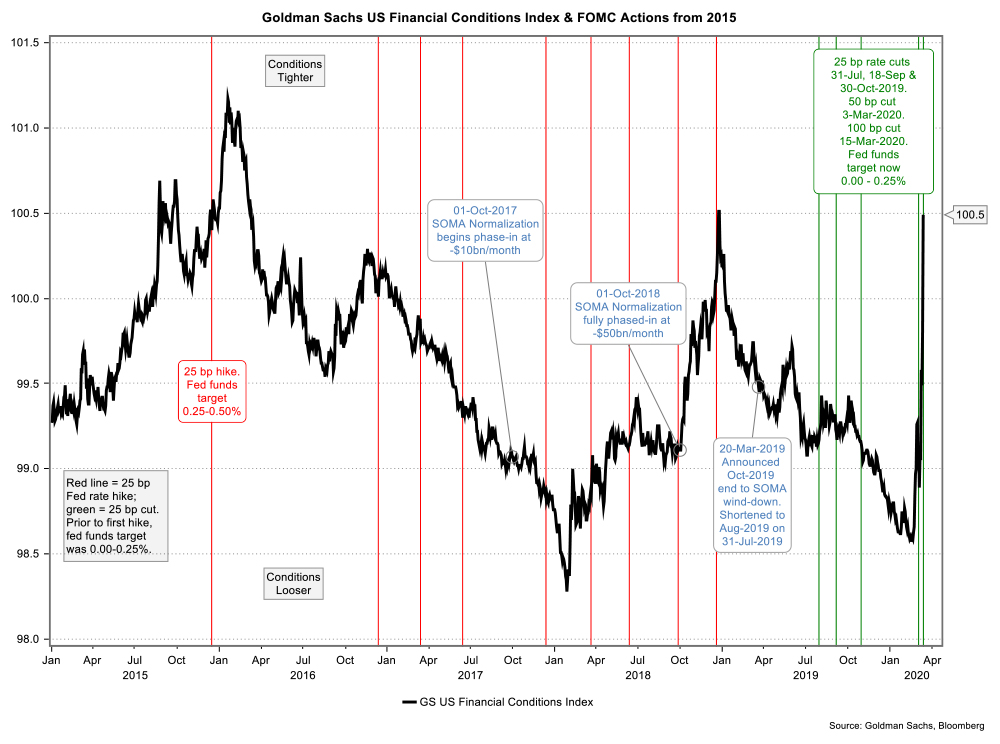

Figure 1: Financial conditions have tightened; Fed pushing back aggressively

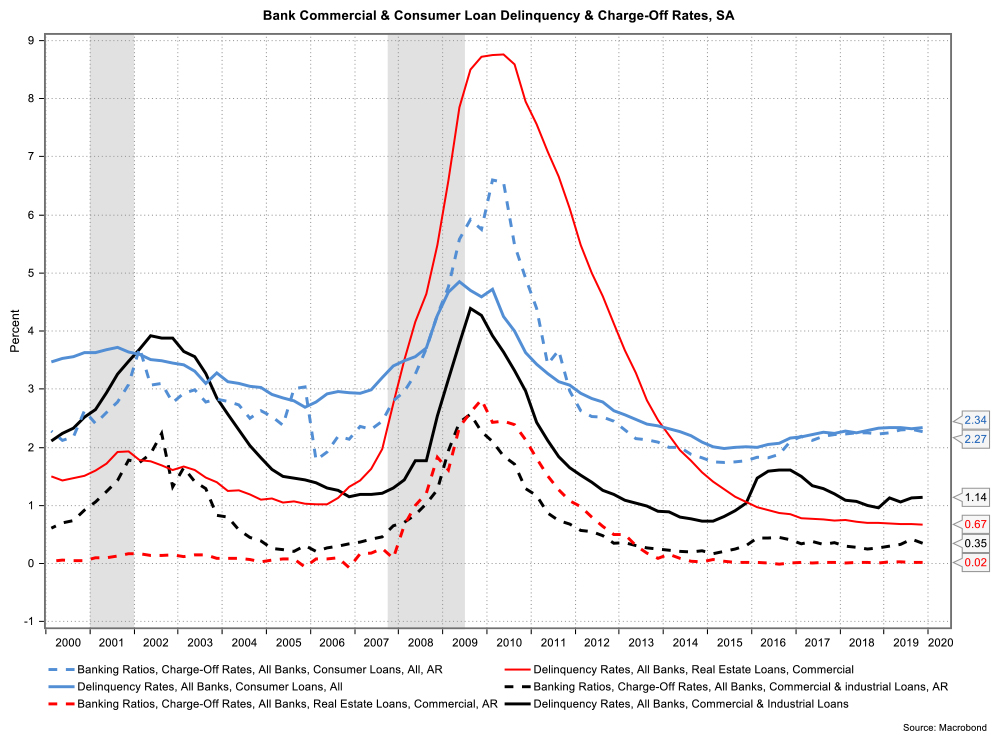

Credit spreads widened dramatically as Treasury rates fell and credit worries intensified. Wider credit spreads and lower stock markets contributed to sharply tighter financial conditions (Figure 1), which the Fed is addressing as discussed above. Among sectors that are important issuers of preferred securities, fundamental credit quality remains solid overall (see our latest Economic Update from February). Energy producers are likely to face major challenges from sharply lower oil and gas prices, but pipeline and midstream companies – which comprise all of our energy investments – have significantly less commodity price exposure than producers and should weather this period of lower energy prices. In contrast, bank balance sheets have rarely looked better. In just one illustration of the health of the US banking system, problem loans are at or near historical lows (Figure 2). We believe banks are well prepared to handle strains from the coronavirus.

Figure 2: Banks’ problem loans hovering at or near historical lows

Prices of nearly all preferred and contingent capital securities are down materially, led by energy names but even among the strongest bank issuers. Nonetheless, we remain confident in the long-term credit quality of issuers in the portfolio. Many companies will see earnings fall, but we expect their ability to pay interest and dividends to remain intact. Risk premiums have jumped well ahead of likely risk, and we see good opportunity for investors willing to ride out this period of uncertainty. We probably need to see new coronavirus cases slow meaningfully before credit markets can stage a substantial rebound. While much depends on how long the shock from coronavirus lasts, as long as firms have available liquidity – and we think the Fed’s support of the banking system will ensure that – then credit spreads could narrow swiftly when market sentiment improves. From current levels, there is a lot of upside in that recovery.

Flaherty & Crumrine Incorporated

© 2020, Flaherty & Crumrine Incorporated. All rights reserved. This commentary contains forward-looking statements. You are cautioned that such forward-looking statements are subject to significant business, economic and competitive uncertainties and actual results could be materially different. There are no guarantees associated with any forecast; the opinions stated here are subject to change at any time and are the opinion of Flaherty & Crumrine Incorporated. Further, this document is for personal use only and is not intended to be investment advice. Any copying, republication or redistribution in whole or in part is expressly prohibited without written prior consent. The information contained herein has been obtained from sources believed to be reliable, but Flaherty & Crumrine Incorporated does not represent or warrant that it is accurate or complete. The views expressed herein are those of Flaherty & Crumrine Incorporated and are subject to change without notice. The securities or financial instruments discussed in this report may not be suitable for all investors. No offer or solicitation to buy or sell securities is being made by Flaherty & Crumrine Incorporated.

[1] Normally, we would view a lower capital buffer as a possible credit concern. In these circumstances, we think it helps prevent a temporary liquidity shortage from triggering a fundamental credit downturn. It’s good policy.

[2] The eight US G-SIBs are JPMorgan Chase, Bank of America, Citigroup, Wells Fargo, Bank of New York Mellon, State Street, Goldman Sachs, and Morgan Stanley.

[3] As of this writing, US fiscal policy actions have been limited in size and scope. We await additional policy responses from Congress and the Administration as the situation evolves.

Destra Capital Investments is providing this update with permission from Flaherty & Crumrine Incorporated. No offer or solicitation to buy or sell securities is being made by Destra Capital Investments.