A Review of 2022 Dodd-Frank Bank Stress Tests

Flaherty & Crumrine, Incorporated

August 31, 2022

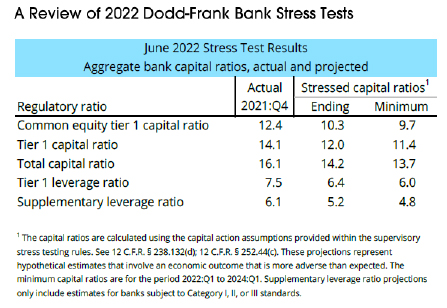

On June 23, the Federal Reserve released its 2022 large-bank Dodd-Frank Act stress test results. They were mostly as expected, and all 33 banks “passed” the 2022 stress test amid the prevailing global economic uncertainty. Under the 2022 “severely adverse scenario”—which factored in unemployment peaking at 10% in 3Q23, real GDP down 6.2%, equities down.

55%, house prices down 28.5% and commercial real estate down 40%—the average minimum common equity Tier 1 (CET1) capital ratio for this year’s 33 bank participants was 9.7% versus 10.6% in the June 2021 test (only 23 banks took the test last year).

The results of this year’s stress test demonstrate that large U.S. banks remain “well-capitalized,” reporting high capital levels, and no bank breached minimum capital requirements during the two-year stress period. Under all scenarios, the 33 large banks maintained capital buffers that were significantly above the Fed’s required minimum, after capital actions. Large U.S. banks are well prepared for a recession, should one arrive, over the next several years.

The Fed also conducted its 2022 Comprehensive Capital Analysis and Review (CCAR) to evaluate bank capital plans in light of the stress tests. Our main CCAR takeaway is that banks continue to exercise discipline regarding common shareholder returns. For example, JPMorgan and Citigroup did not increase their quarterly dividends. At the same time, banks maintain flexibility to increase dividends and share repurchases if earnings accelerate during 2H22 as projected.

Most money center banks will be subject to larger stress capital buffer (SCB) requirements effective October 1, 2022, adding to those banks’ CET1. In particular, Bank of America and Citigroup saw their SCB requirement increase 100 bps from last year’s exam, which will temper both dividend increases and share buybacks. Heading into 2023, we expect these banks to accrete capital and build cushions in their CET1 ratios. Meanwhile, regional banks have more flexibility to raise quarterly dividends and maintain, or even increase, share buyback programs following this year’s stress test, given an expected recovery in C&I (specifically, revolver utilization rates) and commercial R/E lending, as well as sizeable loan loss reserves already in place. Given the increased risk resulting from monetary policy tightening, we expect all banks to maintain conservative capital and loan-loss positions over coming quarters, which should continue to support preferred investors.

Destra Capital Investments is providing this update with permission from Flaherty & Crumrine, Incorporated. No offer or solicitation to buy or sell securities is being made by Destra Capital Investments.