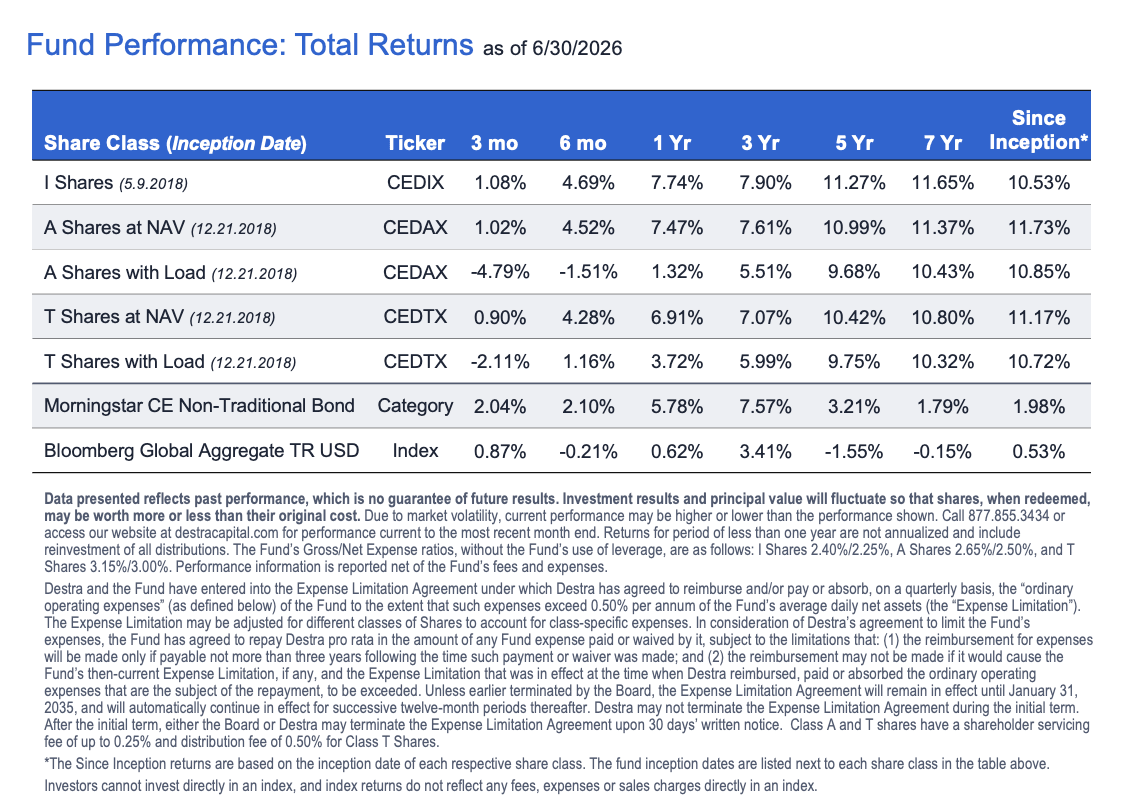

The BlueBay Destra International Event-Driven Credit Fund I Share Class (CEDIX) has been the top performing interval fund8 7-year (11.65%), and since inception7 (10.53%) annualized time periods

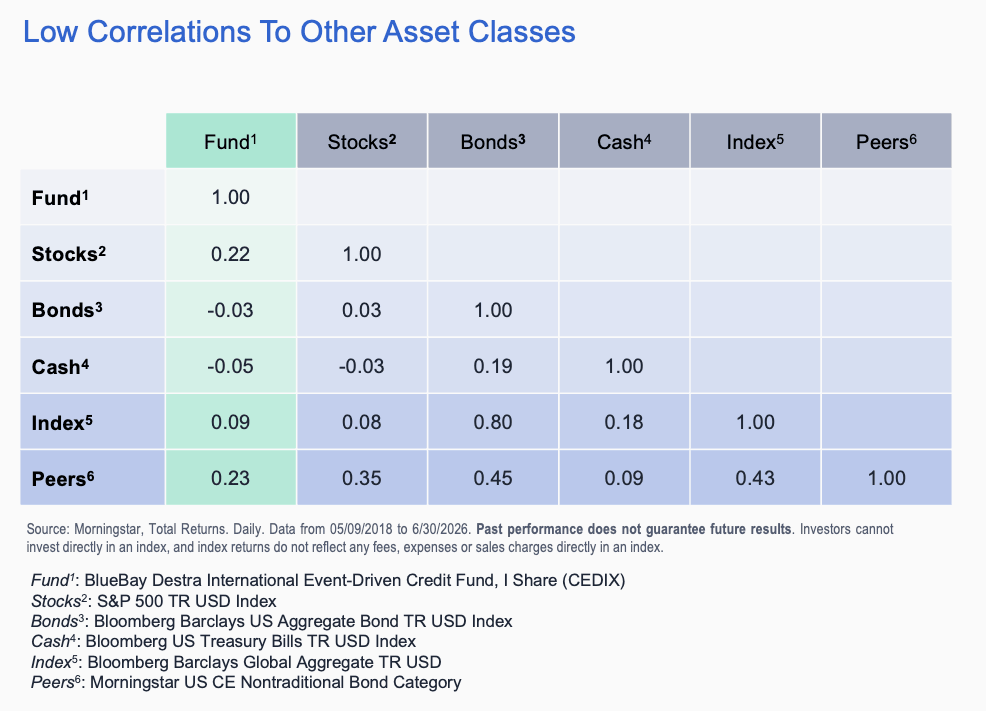

While the Fund boasts impressive returns over the time periods, it also may provide diversification based on its low correlation to other major asset classes such as Stocks2 (+0.22), Bonds3 (-0.03), and Cash4 (-0.05)

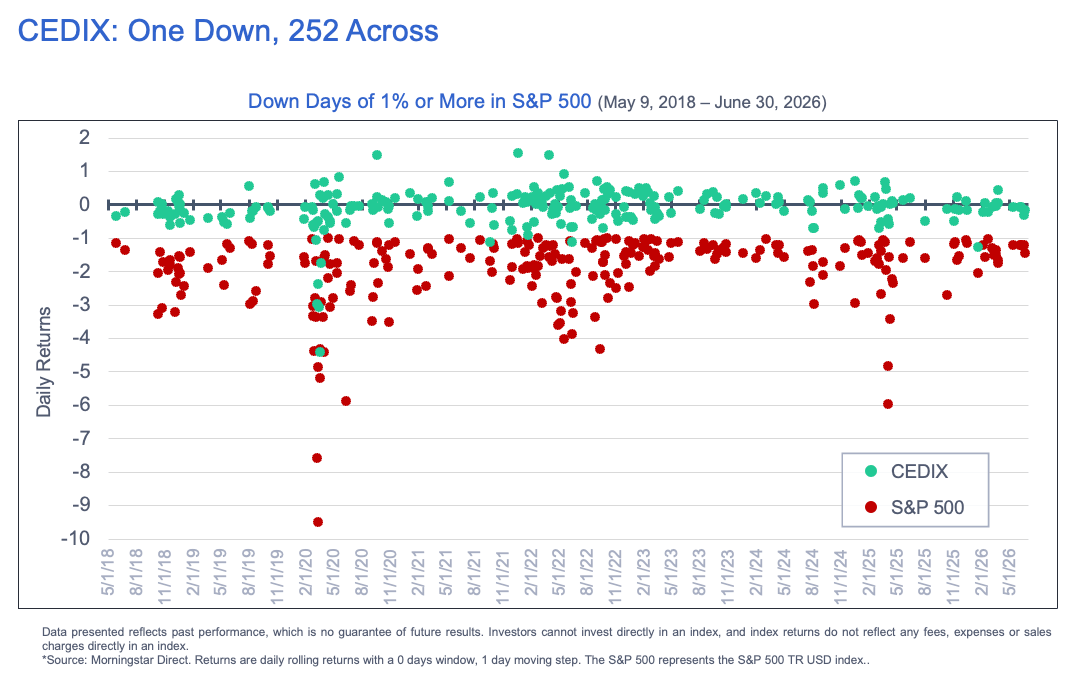

Since Inception of the Fund7, there have been 252 days where the S&P500 has gone down -1% or more. The cumulative return for the S&P500 on those days is -499.38% and the average down day is -1.98%. CEDIX experienced negative returns on only 139 of those days with a cumulative return of -25.46% and an average daily return of -0.10%.

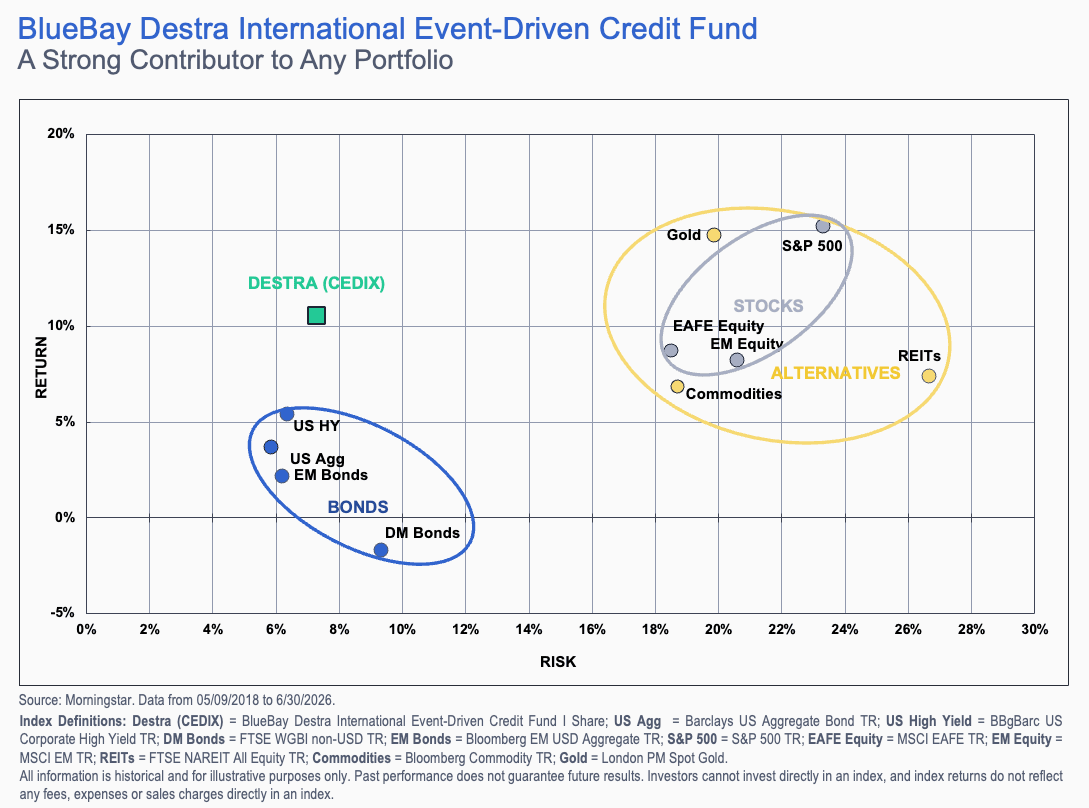

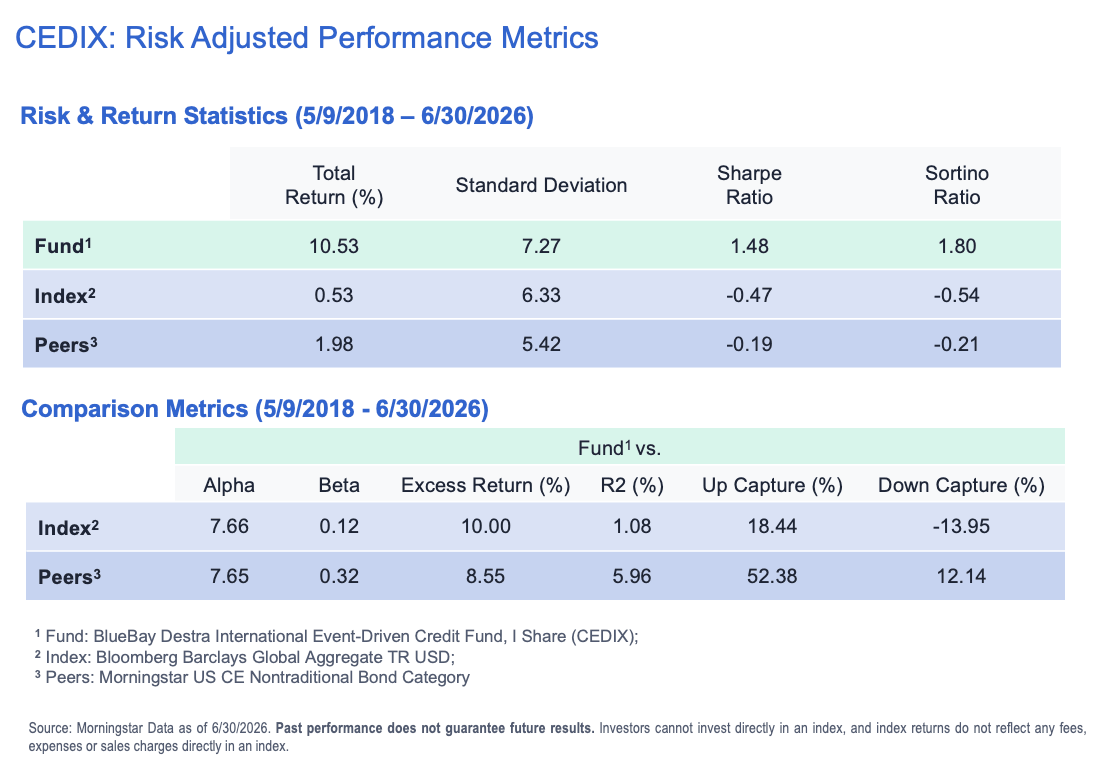

The Fund has delivered superior risk-adjusted returns to Stocks, Bonds, and Alternatives since inception7. Elevate portfolios “Up” (returns) and “to the Left” (risk) with Event-Driven Credit.

The Fund has produced remarkable sharpe and sortino ratios, alphas and excess returns vs a global market reference index (Bloomberg Global Aggregate Bond TR Index) and its Morningstar Peers Category (US CE Nontraditional Bond).

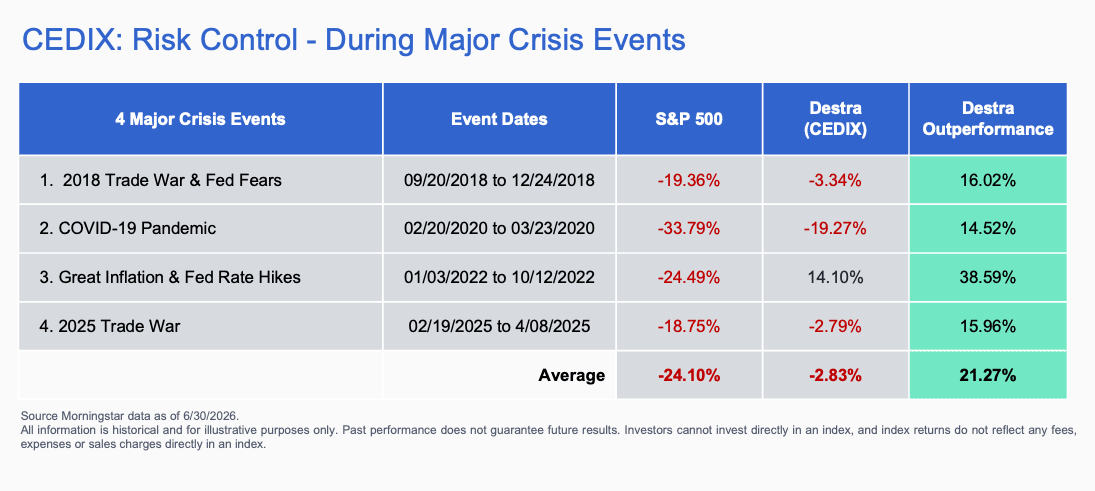

Since inception, CEDIX has demonstrated its ability to provide risk control during major crisis events in relation to the S&P 500 Index. During the 4 major stock market drawdown periods that the Fund has experienced, the S&P 500 average drawdown has been -24.10% vs CEDIX average drawdown of only -2.83%.

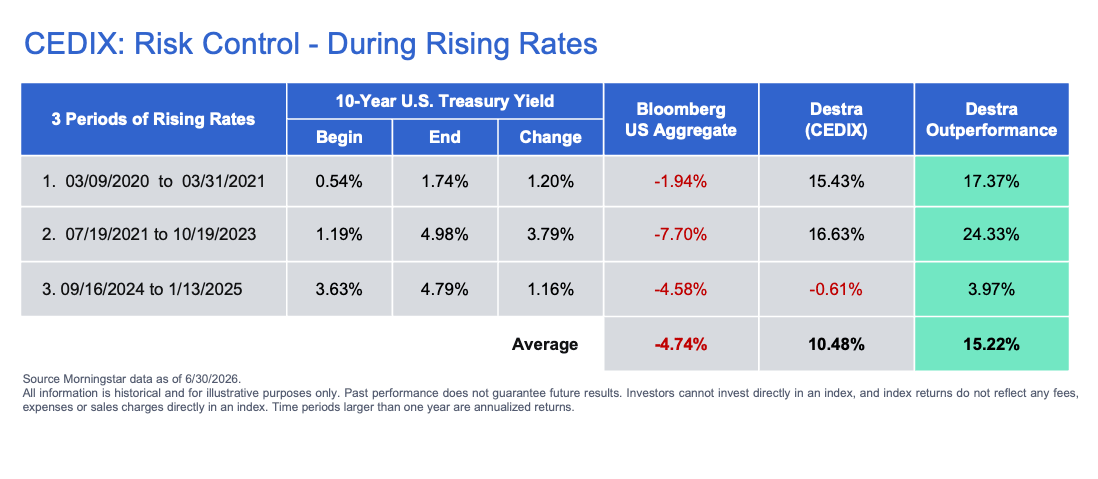

The Fund has also demonstrated its ability to control risk during periods of rising interest rates in relation to the Bloomberg Barclays US Aggregate Bond Index. During the three periods of 100+ bps increases in the 10 Yr Treasury Yield, the Agg has averaged a loss of -4.74% vs CEDIX average return of +10.48%.

Expand Your Horizon: Looking Beyond Traditional Fixed Income

As advisors evaluate portfolio positioning heading in 2026, many are rethinking how traditional fixed income fits within broader asset allocation.

Watch the Expand Your Horizon webcast featuring Dillon Neale, CFA® of RBC BlueBay Asset Management. In this brief, 15-minute session, Dillon explains how experienced credit managers look beyond coupon-focused strategies to identify opportunities in event-driven and opportunistic credit—where price dislocations and identifiable catalysts may contribute to total return.

Submit your contact information to receive the webcast link via email.