A November to Remember!

Destra Capital

December 1, 2023

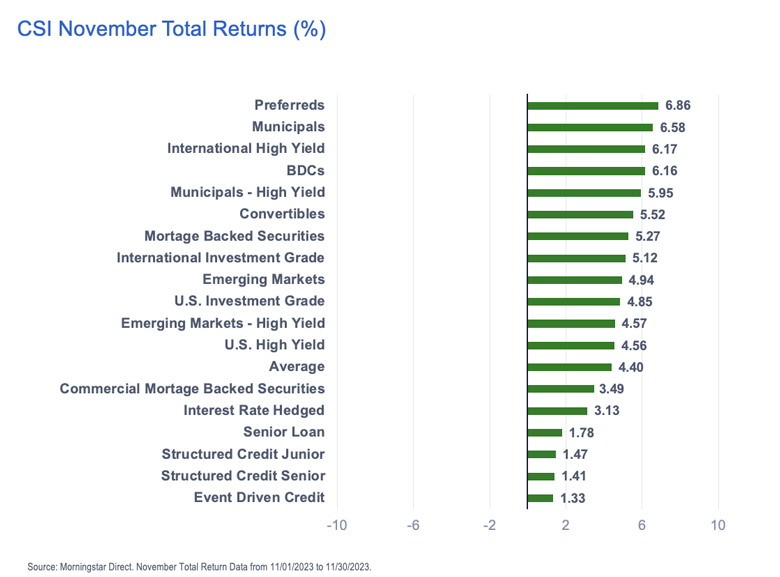

Credit markets (and pretty much all risk assets) rocked the house in November! The Destra Credit Strategies Indicator (“CSI”) was solid green for the month across all 18 categories!

It seemed everywhere you turned in November, it was green on the screen! Preferreds led the way up some 6.86% in the month, followed by Municipals and International High Yield. Talk about a heterogenous mix at the top of the performance charts!

Event Driven Credit was the laggard for the month, up just 1.33%, with Structured Credit taking up the next two spots at 1.41% for the Senior tranche strategies and 1.47% for the Junior.

For long time Credit Event readers you may have noted that we said “18” categories in the intro paragraph. That is because we have expanded the CSI to add an 18th strategy – Convertibles!

With the sustained and persistent rise in rates, new issue convertibles are coming out with something not seen in almost a decade….a current coupon of some note, to go along with the big equity option kicker. Convertibles come into the CSI this month with a bang, up 5.52% for November.

Preferred Outcomes

The best results of the month though, belong to the long beleaguered Preferreds. They were up 6.86% in the CSI, leading all other credit categories. Preferreds have been hit this year with a double-whammy of “perceived” long duration -- though in truth the overall preferred market is intermediate at best -- and the curse of banks going bust. Thanks Silicon Valley and Credit-less Suisse! But that was all in the rear-view mirror for Preferreds this month as the belief that Fed was done raising and might even soon start cutting rates, made the relatively high yields of preferreds attractive again.

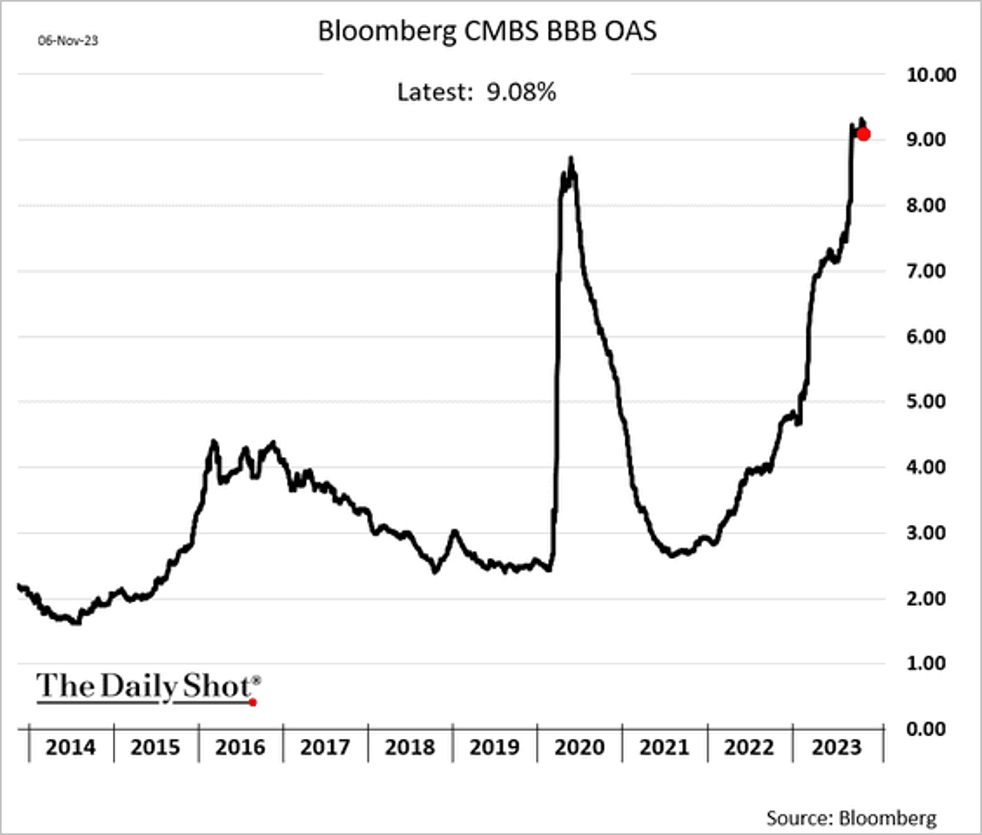

Spread Too Thin?...

…not in the Commercial Mortgage Backed Securities markets. “Spreads are holding at multi-year highs, signaling concerns about commercial property credit,” according to Bloomberg. Despite the concerns, the CMBS category did well in November, up 3.49%. Its cousin, the “residential focused” MBS category did even better, up 5.27%, as US housing prices showed remarkable price resilience, despite a dramatic drop in the number of homes actually sold coast to coast.

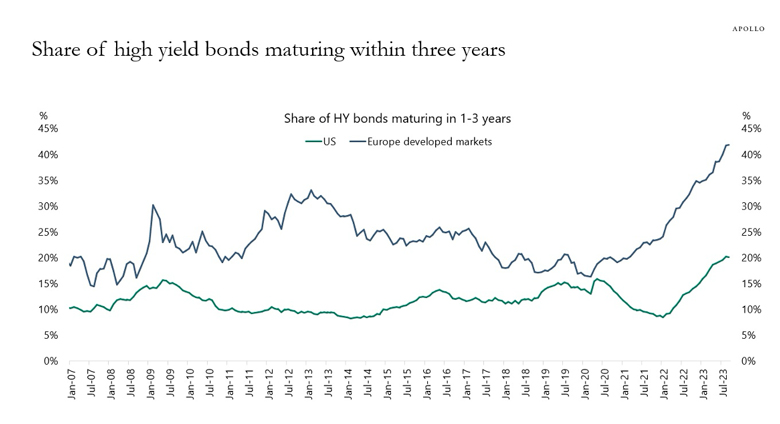

Three Years And Out

International High Yield had a big month, up 6.17%, handily whooping US High Yield at 4.56%. This despite the fact that almost 45% of all European high yield issues will mature in the next 3 years. That is a big “risk on” for investors buying into leveraged companies that are staring into the teeth of the highest refinancing costs in over a decade. According to Torsten Sløk, the Chief Economist at Apollo, “European credit is more vulnerable to higher rates because the share of …HY bonds maturing within three years is higher in Europe than in the US….The bottom line is that Fed hikes and ECB hikes are having a negative impact on credit, but the impact is going to be more significant in Europe, which increases the likelihood of a harder landing in Europe.” Well, tell that to the high yield markets this month, Torsten. They were not listening.

Source: Torsten Sløk, Apollo Chief Economist, November 2, 2023

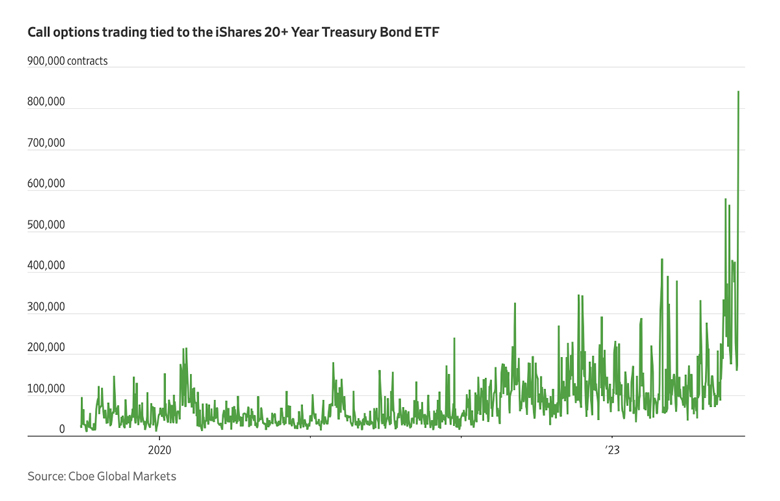

Long and No Longer Wrong! AKA, TLTing at Windmills

There were a few brave “duration hunters” back in the summer and early fall, but they were early. Going out longer on the curve was not really rewarded big here until November. Some investors (ah hem, speculators) were not content to just go long the asset, they had to push their bets….and what better way than to option yourself out? Ah, the old-fashioned option, seems almost quaint here in the age of swaps and fancier derivatives.

The Wall Street Journal noted “Call options trading tied to the iShares 20+Year Treasury Bond Exchange-Traded Fund jumped to a record…. according to Cboe Global Markets. That's a sign people are piling into contracts that would profit if the fund kept rallying…. The fund, known by the ticker symbol TLT, has become one of the hottest investments on Wall Street, with hordes of investors rushing to buy the dip in the ETF.”

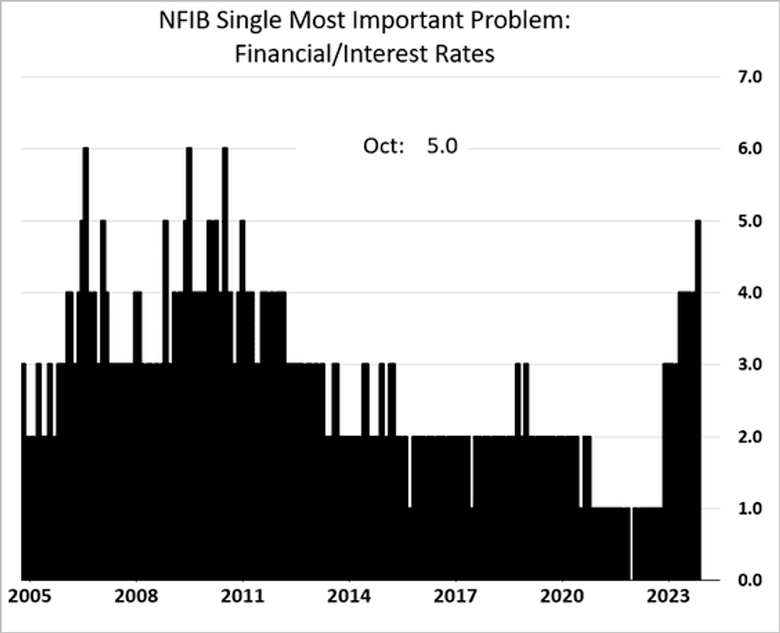

I Got 99 Problems And Refinancing Is One

From the latest NFIB Small Business Sentiment Index in October, more firms are reporting expensive financing as a problem.

Source: NFIB Small Business Sentiment Index, October 2023.

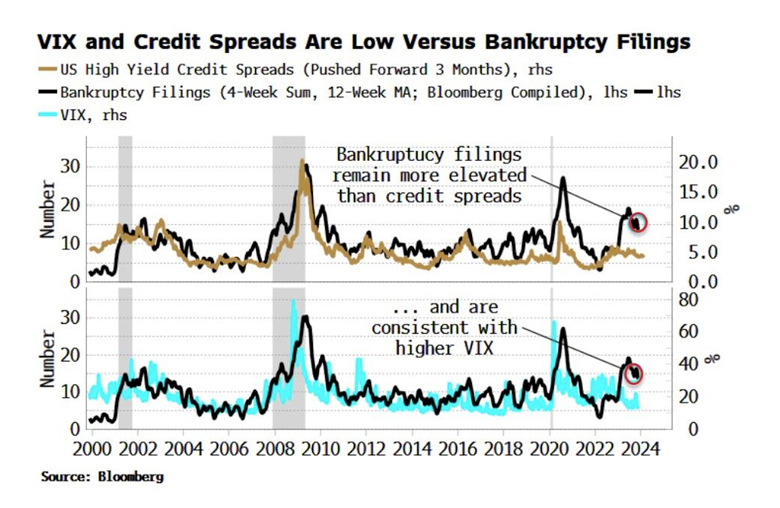

Canary In The Coal Mine

“Underlying credit conditions are not being reflected in credit spreads or implied equity volatility. Both are subject to an abrupt repricing higher when they are.” – Simon White, Zero Hedge.

If Simon White at Zero Hedge is right, the significant increase in bankruptcies is a canary in the coal mine that, at least through November of this year, neither the credit nor the equity markets seem to be worried about.

Keep an eye on High Yield and Senior Loans, at these tight spreads they are priced beyond perfection.

We close out this month’s Credit Events with a great quote from a guy who worked at a bank once…..”Gold is money, everything else is credit,” J.P. Morgan.

See you in December!