A Review of Dodd-Frank Bank Stress Test

Written by Flaherty & Crumrine Incorporated

On June 25, the Federal Reserve released its 2020 large-bank Stress Test results. For the most part, they were as expected given the severity of the current healthcare crisis and global economic slowdown. This year’s “Severely Adverse Scenario” assumptions included (1) U.S. unemployment rate climbing to a peak of 10% in 3Q21; (2) the 10-year Treasury yield slipping to 0.75% during 1Q20 and rising to 2.25% by the end of the stress-test period in 1Q22; (3) equity prices falling 50% through the end of 2020, accompanied by a rise in volatility; and (4) house prices and commercial real estate prices experiencing steep declines of 28% and 35%, respectively, during the first nine quarters of the scenario. As a result, credit cards, commercial real estate and industrial loans showed the largest losses in the severely adverse scenario.

Our main takeaway from this year’s stress test is that most banks remain “well-capitalized” under both the traditional stress test and the Fed’s COVID-19 scenarios. All 33 banks “passed” the 2020 stress test. No banks breached minimum capital requirements during the stress period, although one would need to take small capital actions to do so. This year, in addition to its normal stress test, the Fed included downside scenarios which could result from the pandemic. Under all of these scenarios, all banks maintained capital buffers that were higher than the Fed’s required minimum, after capital actions.

Given heightened uncertainty from COVID-19, the Fed is not allowing large banks to buy back common stock at least through 3Q20 and is limiting quarterly common stock dividends. Preferred dividends are not subject to any of these limitations, although, as always, they could be suspended without triggering an event of default.

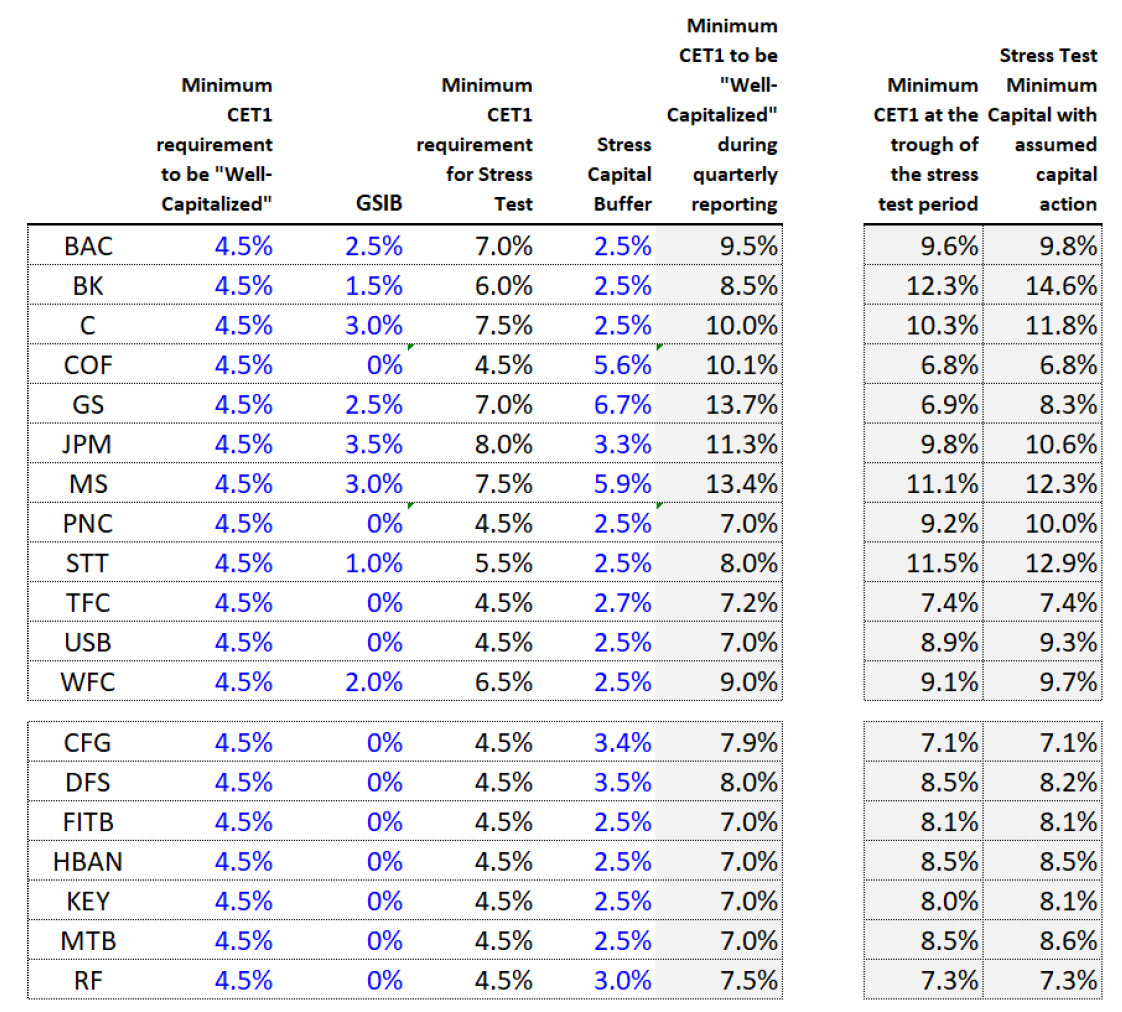

For stress test purposes, the benchmark for a “Well-Capitalized” bank remains common equity Tier 1 (CET1) of 4.5% of risk-weighted assets plus a specific Global Systemically Important Bank Holding Company (GSIB) surcharge, where applicable. The Fed is implementing a new Stress Capital Buffer (SCB) requirement which will take effect in 4Q20. This new buffer was finalized in March 2020 and is independent of the COVID-19 pandemic. It will replace the capital conservation buffer (CCB). Currently, SCBs are either the same as or higher than CCBs they replaced. Importantly, higher levels of common equity capital should help support more senior securities, including preferreds. For quarterly reporting purposes, minimum CET1 for a “Well-Capitalized” bank is the sum of the aforementioned 4.5% plus GSIB surcharge, if any, plus the specific SCB assigned to each individual bank. The table to the right summarizes CET1 requirements and stress test results.

In addition, the Fed will require these large banks to update and resubmit capital plans later in 2020 using updated scenarios to reflect current stresses. In contrast to past years, the Fed will be more proactive and exercise greater vigilance over capital distributions to shareholders (perhaps on a quarter-to-quarter basis) during 2021 as a result of the aforementioned mid-cycle Comprehensive Capital Analysis and Review (CCAR).

Ultimately, the Fed is being deliberate and will assess economic conditions on a more-frequent basis over the next few quarters. Even if the virus and economic conditions worsen over the coming quarters and common stock dividends are cut or suspended next year, such actions would help to conserve common equity capital, which should help support preferred investors.

Destra Capital Investments is providing this update with permission from Flaherty & Crumrine, Incorporated. No offer or solicitation to buy or sell securities is being made by Destra Capital Investments.