Investment Grade Credit – Default Risk, Fallen Angels and Valuations

Originally written by David Riley, Partner, Chief Investment Strategist, BlueBay Asset Management

- The simultaneous supply and demand shock to the global economy from the coronavirus and efforts to contain it is unprecedented in its severity. What is also unprecedented is the scale and speed of the monetary and fiscal policy response that, in our view, will meaningfully mitigate credit stress, especially amongst investment grade-rated companies, many of which are large employers and ‘national champions’ with many dependent local suppliers.

- In our opinion, rating downgrades of companies from investment grade to high yield – so-called ‘fallen angels’ – is by far the more meaningful driver of realised credit losses for investment-grade benchmarked portfolios than investment-grade defaults, which we expect to remain below 1%. The volume of fallen angels will increase over the next few years, in our view, though probably less than in previous peaks during the global financial and eurozone sovereign crises. Moreover, issuers and sectors most at risk from rating downgrades into high yield are already priced as such.

- Extraordinary uncertainty, volatility and the dash for cash currently dominate valuations and fundamentals as the principal drivers of asset prices. An illustration of the dislocation is credit exchange traded funds (ETFs), which experienced greater volatility than the benchmark indices they passively track. Nonetheless, from a historical perspective, investment grade credit spreads are at levels that are typically associated with subsequent positive investment returns.

- In our view, the risk-reward profile for investment grade credit at current valuations is positively skewed for investors over a medium-term horizon. We believe fallen angel risk, rather than default risk, is the primary source of potential credit loss facing investors in investment grade credit, best mitigated, in our opinion, by active strategies able to exploit greater dispersion in returns underpinned by bottom-up credit selection.

The sell-off in growth-sensitive risk assets and volatility in financial markets since late February is unprecedented in its pace and magnitude. Financial markets continue to be roiled by the economic and financial implications of the COVID-19 pandemic and efforts to contain its spread and the loss of life. The world’s major economies are on the brink of recession, the depth and duration of which is highly uncertain.

Credit fundamentals and valuations are currently overwhelmed by volatility across markets, including in core government bonds and commodity prices, as well as the premium placed on liquidity by investors. It is noteworthy that ETFs experienced even greater volatility, with at times large discounts to net asset values (the underlying value of cash bonds) than the credit benchmarks they seek to match. The dramatic widening in credit spreads is to levels that from a historical perspective are associated with a positive skew in subsequent investment returns.

The speed and volatility of the re-pricing of credit in our opinion underscores that the primary driver is exogeneous – the COVID-19 spread and the collapse in oil prices – rather than an unwinding of excessive leverage and financial imbalances that characterised previous crises, including the global financial crisis in 2008-09. If, as we expect, governments and central banks are successful in containing the permanent economic damage from the pandemic, as they are focused on doing with the extraordinary policy measures so far announced, we believe the economic recovery and rebound in markets should be faster than from previous recessions and default cycles.

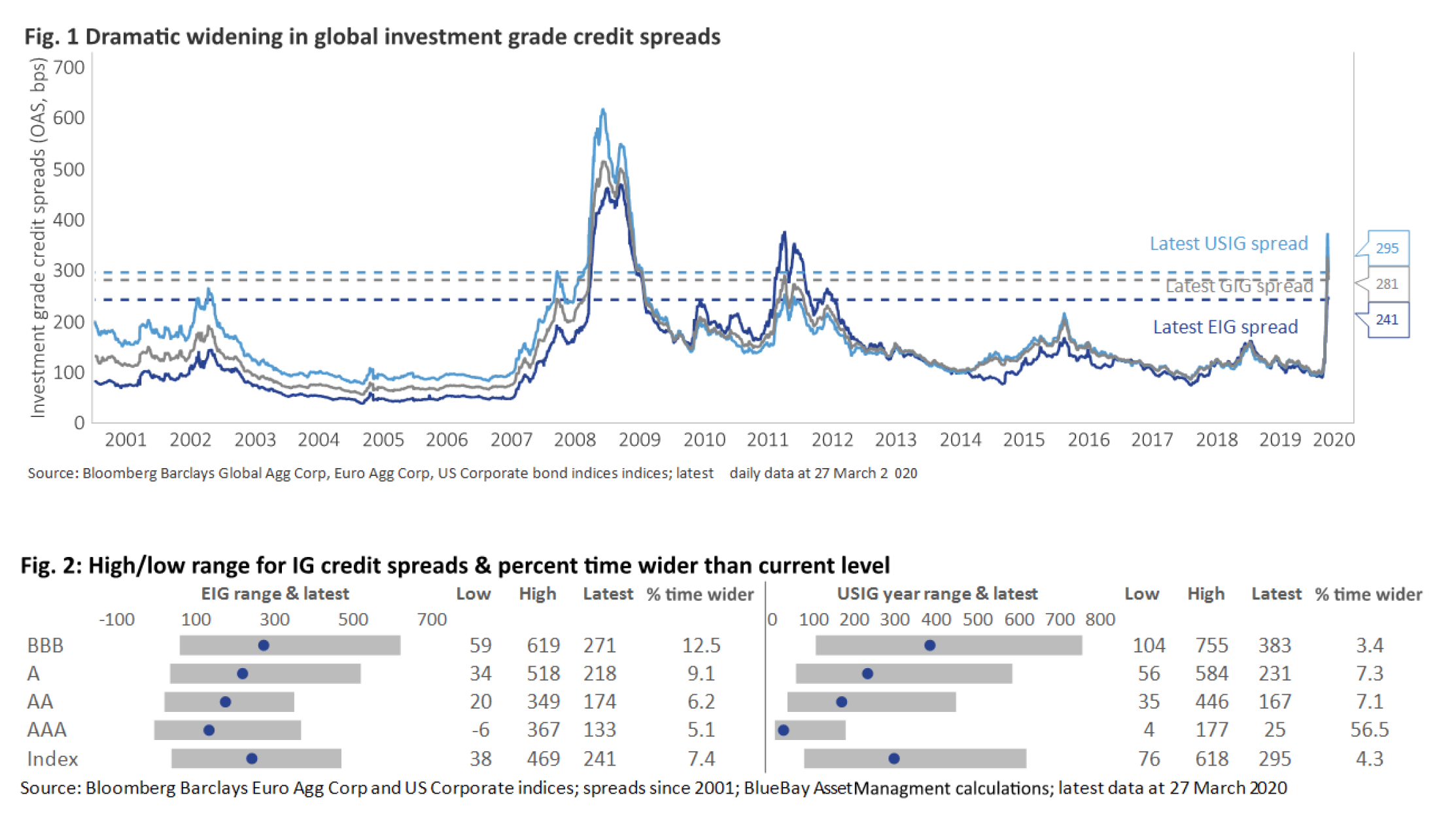

Credit spreads reach crisis wides at record speed

The widening in global investment grade corporate credit spreads over the last month is the most dramatic in the market’s history; spreads are currently at levels only exceeded at the height of the global financial crisis. The widening in European investment grade (EIG) spreads is dramatic, but less severe than for US investment grade (USIG), despite Europe currently being at the epicentre of the global pandemic and with weaker economic fundamentals.

In our view, this reflects greater ‘fallen angel’ risk facing USIG, in part because of the greater presence of energy companies and the purchases and substantial holdings of Euro corporate bonds by the European Central Bank (ECB) even before the crisis erupted. As illustrated in Figures 1 & 2 below, credit spreads on investment grade have rarely exceed current levels.

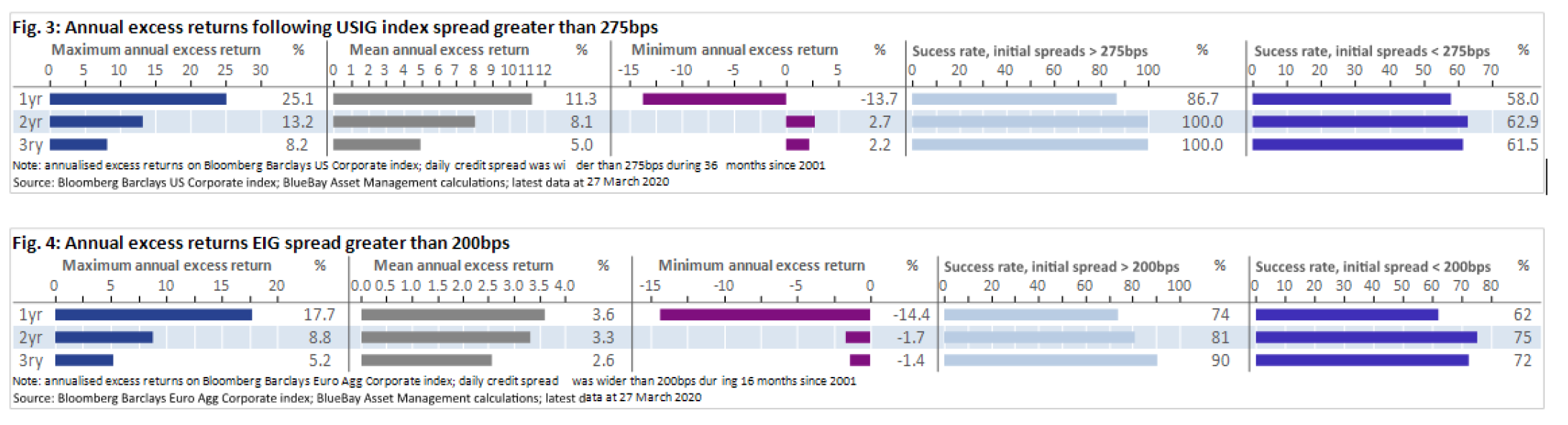

History shows that positive excess returns (i.e. the return over and above similar maturity ‘risk-free’ government bonds) have followed credit spreads at current levels over a one to three-year investment horizon for USIG. For EIG, the ‘success rate’ – the percentage of periods when credit spreads have been at or exceeded current levels – have similarly been followed by positive excess returns over the one and two-year investment horizon and approximately 95% of the time over a three-year horizon.

In Figures 3 & 4, the one, two and three-year subsequent excess returns are shown with an initial credit spread of 275bps and 200bps respectively for USIG and EIG, around 50bps lower than current levels (as at 27 March 2020). Lower than current levels have been chosen for this analysis simply to allow some valuation cushion for the timing of investors’ entry points for deploying new capital into the investment grade market. Even at meaningfully lower entry points on credit spreads than prevailing today, the relative success rate for positive returns when spreads have been above and below these levels demonstrates that from an historical perspective, the current risk-reward profile for investment grade credit appears positively skewed, in our view.

The one-year negative excess returns on US and Euro investment grade credit were incurred in early 2009 following the explosion in credit spreads after the bankruptcy of Lehman Brothers in September 2008.

The Eurozone sovereign debt crisis in 2010-12 also resulted in episodes of negative excess returns in the subsequent two and three-year periods after EIG credit spreads first exceeded 200bps. In our view, the ECB’s EUR750 billion Pandemic Emergency Purchase Programme (PEPP), in addition to its previously announced EUR120 billion asset purchases (QE), has seemingly removed the tail risk that the health crisis could trigger a resumption of the Eurozone sovereign debt crisis.

Our fundamental analysis implies that the failure of a US or European bank is, theoretically, extremely low. Banks are much better capitalised than in 2007 and are playing a crucial role with the support of central banks and governments in providing liquidity and capital to the real economy to cushion the economic shock of the coronavirus.

Default risk and fallen angels

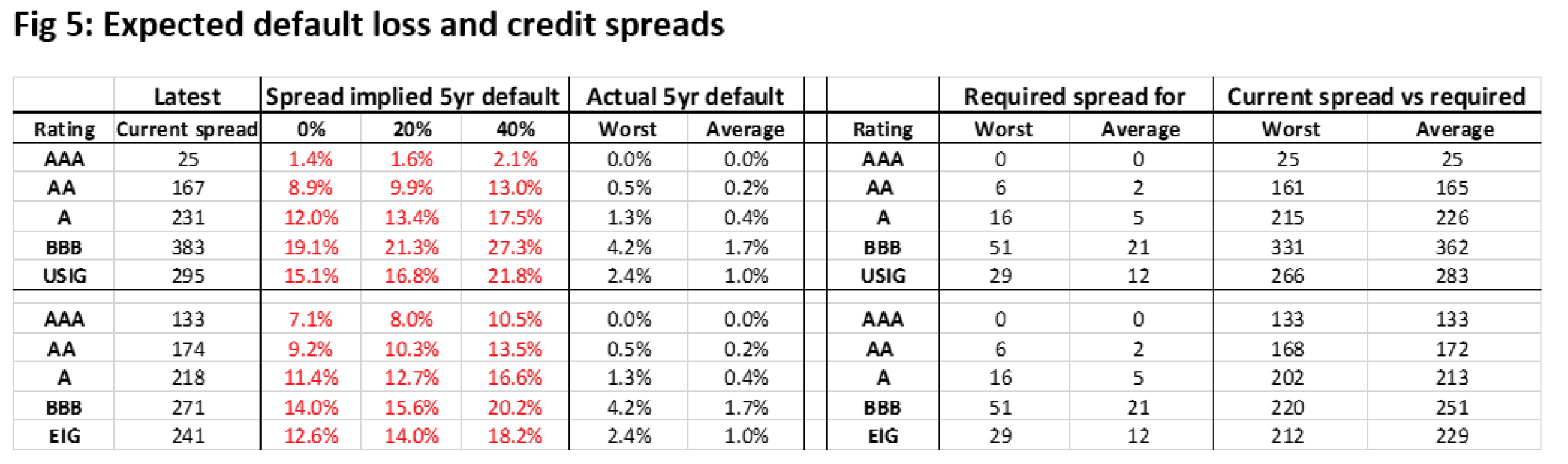

The additional yield over ‘risk-free’ government bonds – the credit spread – for corporate bonds compensates investors for the credit loss from defaults and the greater uncertainty and volatility in returns. The average annual default risk on investment-grade rated corporate debt is historically extremely low. According to Moody’s, the average default rate for investment grade-rated issuers is under 0.1% and under 1% over a one and five-year period respectively, compared to 4% and 19% respectively for sub-investment grade (high yield) borrowers. The annual default rates for investment grade by debt outstanding (rather than as percent of issuers) during the recession and credit downturns of 2001-02 and 2008-09 was around 1.5, according to a February 2020 Moody’s study.

As shown in Figure 5, current credit spreads far exceed even the worst historical episodes of investment grade defaults over a 5-year horizon.

Note: S&P average and worst cumulative 5-year default rate, 1983-2017

Source: credit spreads by rating from Bloomberg Barclays US Corporate and Euro Agg Corporate indices; S&P; and BlueBay Asset Management calculations; spreads at 27 March 2020

The rare occasions when investment-grade companies ‘jump to default’ is invariably due to idiosyncratic events, often the revelation of accounting fraud (for example, Parmalat bankruptcy in 2003). This underscoring the importance of incorporating the ‘G’ in ESG – governance – as well as social and environmental factors, into the investment process.

The unprecedented collapse in revenues from the virus-induced economic lockdown will place severe financial pressure on many companies, including those rated investment grade. In our view, those with liquidity buffers and robust balance sheets will be best placed to absorb this pressure.

The policy measures announced by governments, such as the EUR600bn ‘rescue fund’ launched in Berlin and the several hundred billion set aside for providing loans to US companies in the USD2 trillion fiscal package recently passed by Washington, are intended to provide liquidity to the corporate sector. French President Macron went as far as to state in a television address to the nation that “no French company whatever its size will be exposed to the risk of collapse” due to the coronavirus crisis.

However, investors also demand additional yield to compensate for the risk of rating downgrades.

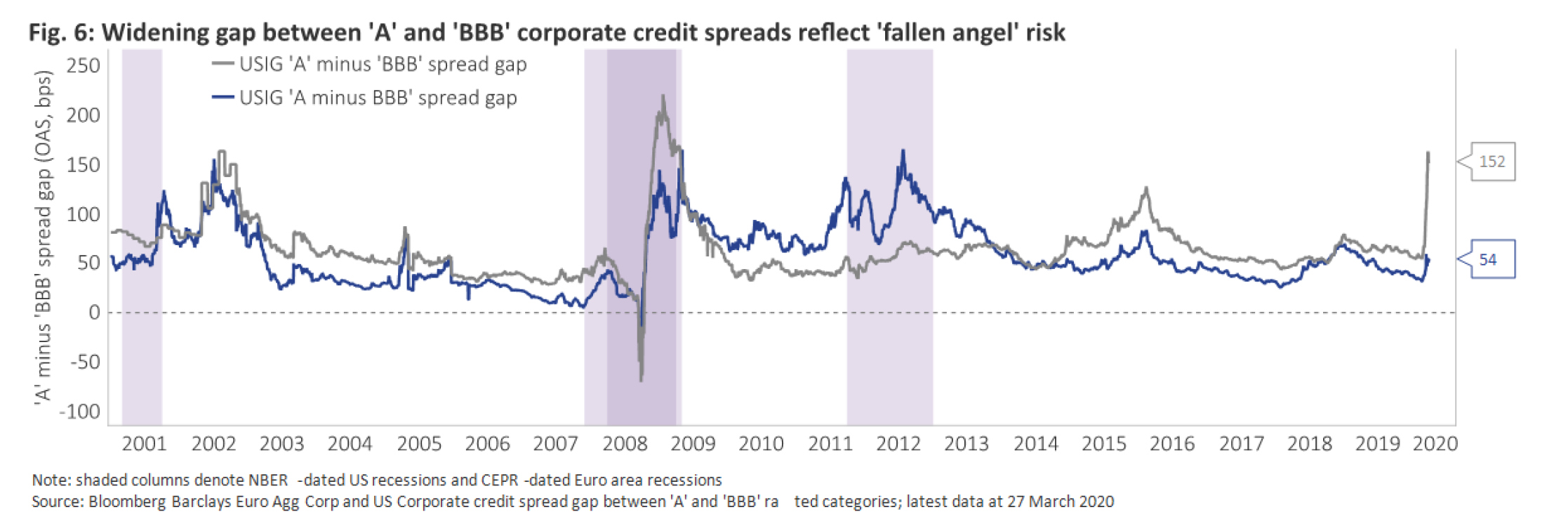

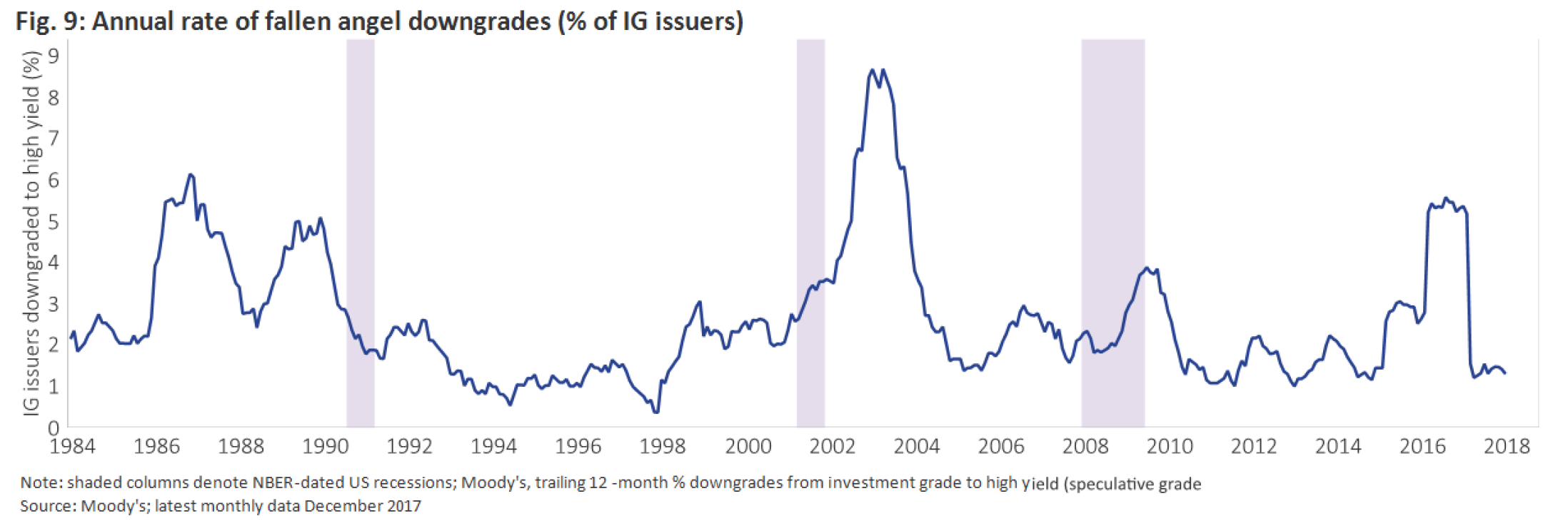

Most realised credit losses in a benchmarked investment grade portfolio come from selling bonds that drop out of the index when they are downgraded into high yield – ‘fallen angels’ – rather than from defaults. We feel the widening spread between A and BBB-rated bonds indicates that investors are anticipating a meaningful increase in the number of fallen angels, especially in the US.

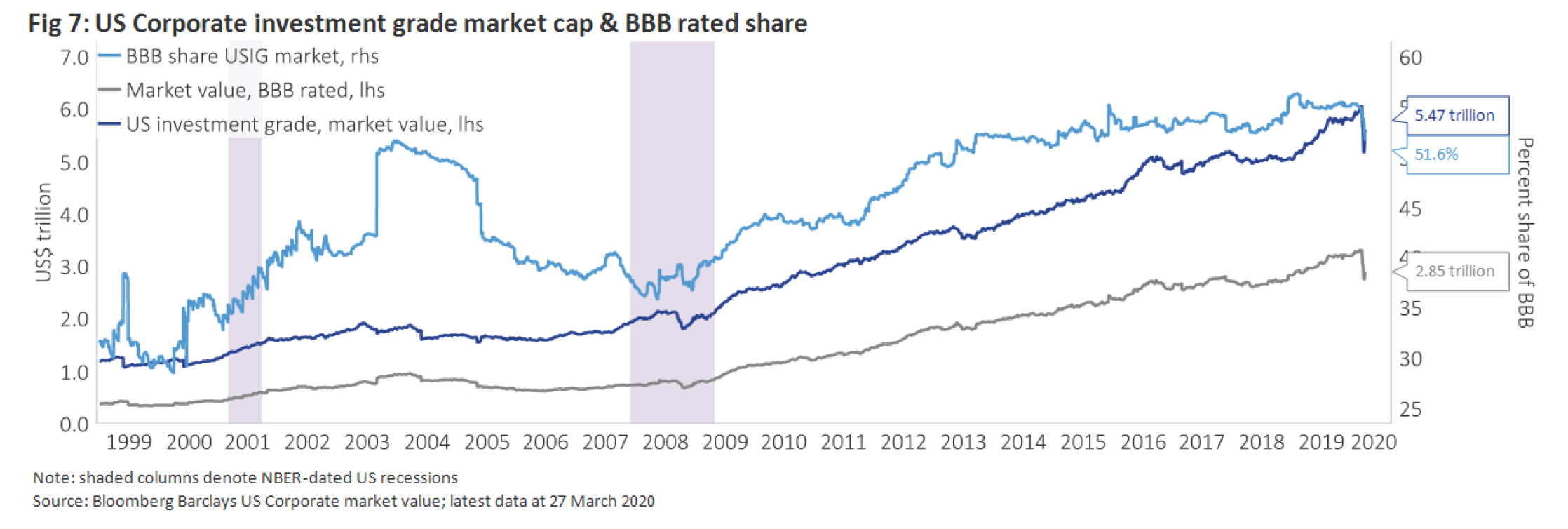

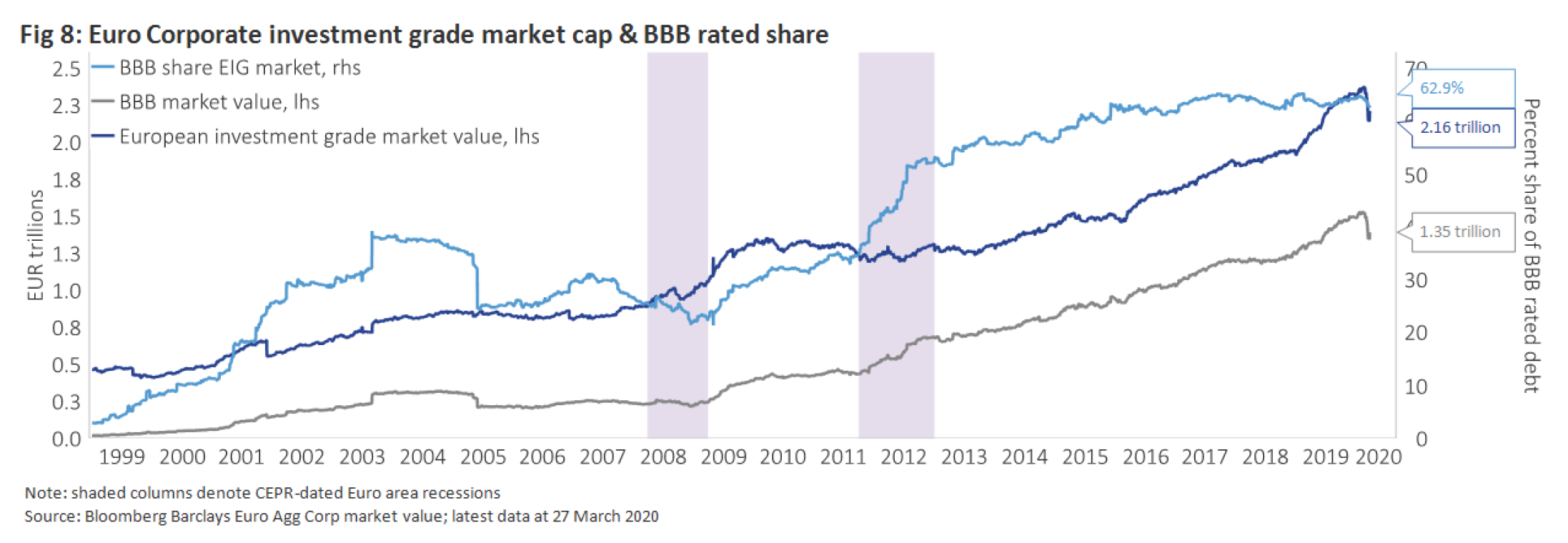

The rating mix of the investment grade market in the US and Europe has deteriorated since the global financial crisis.

In the US, we believe this is because higher-rated companies used cheap debt in the post global financial crisis era to fund share buybacks. Many CEOs chose a capital structure with a lower credit rating rather than credit rating downgrades reflecting a secular deterioration in business profiles.

In Europe, we believe the rise in the ‘BBB’ share was, in part, due to the counterpart of widespread sovereign rating downgrades during the 2010-12 Eurozone crisis, rather than an increase in leverage. The current market value of ‘BBB’-rated debt – the lowest investment-grade rating bucket most at risk of rating downgrade into high yield – is around USD2.9 trillion and EUR1.4 trillion – 52% and 63% respectively of the current market value of the US and Euro investment grade corporate bond markets.

On average, the annual rate of investment-grade rated companies that are downgraded to high yield is around 2.5% and is typically matched by ‘rising stars’ being upgraded from sub-investment grade.

Downgrade and fallen angel rates did pick-up in past recessions, but not meaningfully so. The worst years for fallen angels were not during a recession, but in the early 2000s following the bursting of the ‘dot-com’ bubble and several cases of accounting fraud (such as Enron and WorldCom).

In our view, downgrade risk is meaningfully higher than it was, but the magnitude of fallen angels will depend on the duration of the recession and the success of policy measures intended to limit the economic damage. The latest US fiscal support package includes USD500 billion in capital for supporting business, including additional equity that the Federal Reserve can leverage to increase the scale of its corporate bond purchases and loans, potentially into the trillions of dollars.

In Europe, the ECB backstop for European investment grade credit is extremely powerful. Under the PEPP and its existing QE programme, the ECB is likely to be buying some EUR20-30 billion per month of corporate credit, taking their holdings to some EUR300-400 billion by year-end. This is 30+% of outstanding non-financial eligible corporate debt.

We assess that a conservative range for the volume of US investment grade debt that could fall into high yield over the next two years is between USD200 billion and USD300 billion. The upper-end of the range would be similar to the experience of the global financial crisis and ‘great recession’, when the cumulative fallen angel rate over the two years (2008-09) was just under 10% for BBB-rated nonfinancial corporate issuers, according to S&P Global Market Intelligence research.

The sectors we believe are most at risk of downgrades are autos, energy & mining and consumer discretionary and this is already reflected in bond prices. The average price of BBB-rated energy bonds is just 80 cents and 90 cents for consumer cyclicals companies (according to Bloomberg as at 26 March). In our view, current valuations in US investment grade already factor in a meaningful wave of rating downgrades and fallen angels.

European fallen angel bonds peaked around EUR80 billion in 2009 and in the eurozone sovereign crisis. Considering the scale of the ECB backstop and governments focus on providing support to European companies, we think the volume of fallen angel debt will be in the range of EUR50–100 billion (roughly between 5% and 10% of Euro non-financial corporate bonds currently rated in the BBB bucket).

A severe but relatively short recession, with extraordinary policy support providing a funding bridge to recovery, implies a lower incidence of investment grade corporate defaults and fallen angels than otherwise would be the case, in our view, considering the severity of the economic downturn.

We anticipate that the default rate for high yield (sub-investment grade rated issuers) will rise sharply from their current historic lows – high yield credit spreads currently factor in double-digit default rates – but we believe it is fallen angels rather than defaults that pose the key risk for the investment grade corporate market, as we outlined in our 23 March article ‘High yield credit – valuations and returns from a historical perspective’.

Summary

The global pandemic and associated economic shock is unprecedented, but so has been the scale and speed of the policy response by governments and central banks. The focus of policymakers is to minimise the permanent loss of productive capacity by providing companies with financial support to bridge them until we come out on the other side of the virus. Investment grade companies are typically large employers – many are ‘national champions’ that are crucial to domestic supply chains and if required, will in our view benefit from public financial assistance. We believe the scale of the policy support will meaningfully mitigate the negative impact on the investment grade credit market, especially from default risk, from the economic shock of the pandemic and the efforts to contain it.

We anticipate that default rates will rise dramatically from recent historic lows but will be very heavily concentrated in already sub-investment grade rated highly leveraged companies. We expect default risk in investment grade to remain very low and for the primary source of potential credit loss for investors tightly constrained by indices to come from the forced selling of fallen angels.

In our view, rising fallen angel risk is reflected in current wide credit spreads and is best mitigated by investment strategies that do not passively track benchmark indices and hence are able to activity exploit dispersion in returns based on bottom-up credit selection and are not immediate ‘forced sellers’ of the debt of fallen angels.

We believe the dramatic widening in credit spreads more than fully compensates investors in investment grade corporate credit for default risk and a meaningful rise in the volume of fallen angels is reflected in current valuations. History suggests that at current spread levels, investors typically receive positive excess (and total) returns over a one to three-year investment horizon. In our view, the risk-reward profile for investment grade credit is skewed favourably for investors.

This document is issued in the United Kingdom (UK) by BlueBay Asset Management LLP (BlueBay), which is authorised and regulated by the UK Financial Conduct Authority (FCA). BlueBay is also registered with the US Securities and Exchange Commission (SEC) and is a member of the National Futures Association (NFA) as authorised by the US Commodity Futures Trading Commission (CFTC). This document may also be issued in the United States by BlueBay Asset Management USA LLC which is registered with the SEC and the NFA. In Japan, by BlueBay Asset Management International Limited which is registered with the Kanto Local Finance Bureau of Ministry of Finance, Japan. In Switzerland, by BlueBay Asset Management AG where the Representative and Paying Agent is BNP Paribas Securities Services, Paris, succursale de Zurich, Selnaustrasse 16, 8002 Zurich, Switzerland. The place of performance is at the registered office of the Representative. The courts of the registered office of the Swiss representative shall have jurisdiction pertaining to claims in connection with the distribution of shares in Switzerland. In Germany, BlueBay is operating under a branch passport pursuant to the Alternative Investment Fund Managers Directive (Directive 2011/61/EU). In Australia, BlueBay is exempt from the requirement to hold an Australian financial services licence under the Corporations Act in respect of financial services as it is regulated by the FCA under the laws of the UK which differ from Australian laws. In Canada, BlueBay is not registered under securities laws and is relying on the international dealer exemption under applicable provincial securities legislation, which permit BlueBay to carry out certain specified dealer activities for those Canadian residents that qualify as "a Canadian permitted client”, as such term is defined under applicable securities legislation. The registrations and memberships noted should not be interpreted as an endorsement or approval of any of the BlueBay entities identified by the respective licensing or registering authorities. Unless otherwise stated, all data has been sourced by BlueBay. To the best of BlueBay’s knowledge and belief this document is true and accurate at the date hereof. BlueBay makes no express or implied warranties or representations with respect to the information contained in this document and hereby expressly disclaim all warranties of accuracy, completeness or fitness for a particular purpose. The document is intended only for “professional clients” and “eligible counterparties” (as defined by the FCA) or in the US by “accredited investors” (as defined in the Securities Act of 1933) or “qualified purchasers” (as defined in the Investment Company Act of 1940) as applicable and should not be relied upon by any other category of customer. In Hong Kong, the Fund is not authorised by the Securities and Futures Commission for sale to the retail public and this document is only available for professional investors (as defined in the Securities and Futures Ordinance (Cap 571)) only. This document does not constitute an offer to sell or the solicitation of an offer to purchase any security or investment product in any jurisdiction and is for information purposes only. This document is not available for distribution in any jurisdiction where such distribution would be prohibited and is not aimed at such persons in those jurisdictions. Except where agreed explicitly in writing, BlueBay does not provide investment or other advice and nothing in this document constitutes any advice, nor should be interpreted as such. No BlueBay Fund will be offered, except pursuant and subject to the offering memorandum and subscription materials. This document is for general information only and is not a complete description of an investment in any BlueBay Fund. If there is an inconsistency between this document and the offering materials for the BlueBay Fund, the provisions in the Offering Materials shall prevail. Past performance is not indicative of future results. The investments discussed may fluctuate in value and investors may not get back the amount invested. You should read the offering materials carefully before investing in any BlueBay fund. While gross of fee figures would reflect the reinvestment of all dividends and earnings, it would not reflect the deduction of investment management and performance fees. An investor’s return will be reduced by the deduction of applicable fees which will vary with the rate of return on the fund. For example, if there was an annualised return of 10% over a 5-year period then the compounding effect of a 0.60% management fee and a 0.20% performance fee would reduce the annualised return to 9.32% (figures used are only to demonstrate the effect of charges and are not an indicator of future performance). In addition, the typical fees and expenses charged to a fund will offset the fund’s trading profits. A description of the specific fee structure for each BlueBay strategy is contained in the fund’s prospectus. Net performance figures reflect the reinvestment of all dividends and earnings, and the deduction of fees and expenses. No part of this document may be reproduced in any manner without the prior written permission of BlueBay. In the United States, this document may be provided by RBC Global Asset Management (U.S.) Inc. ("RBC GAM-US"), an SEC registered investment adviser. In Asia, this document may be provided by RBC Global Asset Management (Asia) Limited, which is registered with the Hong Kong Securities and Futures Commission. RBC Global Asset Management (RBC GAM) is the asset management division of Royal Bank of Canada (RBC) which includes BlueBay, RBC GAM-US, RBC Global Asset Management (Asia) Limited and RBC Global Asset Management Inc., which are separate, but affiliated corporate entities. Copyright 2020 © BlueBay, is a wholly-owned subsidiary of RBC and BlueBay may be considered to be related and/or connected to RBC and its other affiliates. ® Registered trademark of RBC. RBC GAM is a trademark of RBC. BlueBay Asset Management LLP, registered office 77 Grosvenor Street, London W1K 3JR, partnership registered in England and Wales number OC370085. The term partner refers to a member of the LLP or a BlueBay employee with equivalent standing. Details of members of the BlueBay Group and further important terms which this message is subject to can be obtained at www.bluebay.com. All rights reserved.

This material has been provided to Destra Capital Investments by a third party. We believe all of the information to be factually correct, however it is subject to change without notice. The opinions presented are of the third party that has provided the information and may not be the opinions of Destra Capital investments.

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy or sell securities, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investor, or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with his or her advisors.